This notebook demonstrates how to obtain the saving rate of a forward-looking consumer using HARK.

# Preliminaries

from HARK.ConsumptionSaving.ConsIndShockModel import (

PerfForesightConsumerType,

) # Import the consumer type

import matplotlib.pyplot as plt

import numpy as np

def mystr(number):

return "{:.4f}".format(number)

# These last two will make our charts look nice

plt.style.use("seaborn-v0_8-darkgrid")

palette = plt.get_cmap("Dark2")1. Creating an agent¶

We now import the HARK class that represents a perfect-foresight consumer with CRRA utility, and create an instance of it with the parameters we’d like.

# Set up a HARK Perfect Foresight Consumer called PFsavrate

# Now we need to "fill" our consumer with parameters that allow us to solve the consumer's problem

# First we need to set out a dictionary

ρ = CRRA = 2.0 # Coefficient of relative risk aversion

Rfree = 1.03 # Interest factor on assets

β = DiscFac = 0.97 # Intertemporal discount factor

LivPrb = [1.0] # Survival probability

Γ = PermGroFac = [1.01] # Permanent income growth factor

# Number of agents of this type (only matters for simulation# Number of periods in the cycle for this agent type

AgentCount = 1

cycles = 0 # Agent is infinitely lived

T_cycle = 1 # Every period is the same

# Make a dictionary to specify a perfect foresight consumer type

dict_wealth = {

"CRRA": CRRA,

"Rfree": [Rfree],

"DiscFac": DiscFac,

"LivPrb": LivPrb,

"PermGroFac": PermGroFac,

"AgentCount": AgentCount,

"cycles": cycles,

"T_cycle": T_cycle,

}

# Now lets pass our dictionary to our consumer class

PFsavrate = PerfForesightConsumerType(**dict_wealth)2. Solving the consumer’s problem and finding the saving rate.¶

The next step is to ask HARK to solve the agent’s optimal consumption problem. The result, or what we call “solution”, is a function cFunc that tells us what is the optimal amount to consume at each level of normalized market resources.

The next cell solves the agent and tests the function

PFsavrate.solve()

test_m = 4

test_c = PFsavrate.solution[0].cFunc(test_m)

print(

"When normalized market resources are m={}, the agent's normalized consumption should be c={}".format(

test_m, test_c

)

)When normalized market resources are m=4, the agent's normalized consumption should be c=1.611193200855211

We are now ready to think about the saving rate of the consumer.

Remember that the saving rate of an agent at time is

Expected 'EOF', got '_' at position 97: …ext{Consumption_̲t}}{\text{Capit…

\text{Saving Rate}_t = \frac{\text{Capital Income}_t + \text{Labor Income}_t - \text{Consumption_t}}{\text{Capital Income}_t + \text{Labor Income}_t}Dividing both the numerator and denominator by the agent’s permanent income and adopting the notation in the course’s lecture notes we have

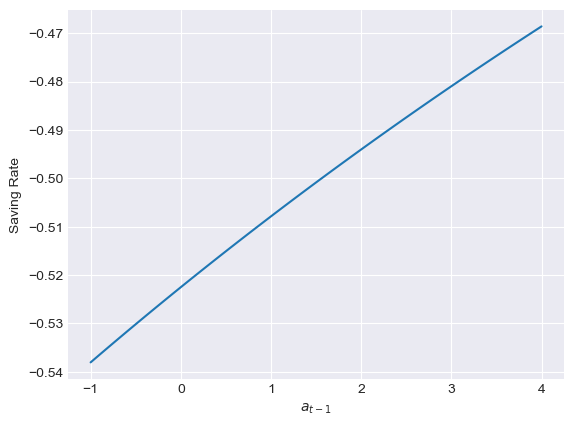

We now have an expression for the saving rate as a function of the previous period’s end-of-period normalized assets . The cell below calculates and plots this relationship for different levels of .

# Create a grid for a

a_tm1 = np.linspace(-1, 4)

# Compute income components at every a

cap_income_t = a_tm1 * (Rfree - 1) / Γ

lab_income_t = 1

# and market resources

m_t = a_tm1 * Rfree / Γ + 1

# Consumption

c_t = PFsavrate.solution[0].cFunc(m_t)

# and finally the saving rate

ς_t = sav_rate_t = (cap_income_t + lab_income_t - c_t) / (cap_income_t + lab_income_t)

# And now the plot

plt.plot(a_tm1, sav_rate_t)

plt.xlabel(r"$a_{t-1}$")

plt.ylabel("Saving Rate")