Portfolio Choice with Risky Housing

December 15, 2021

Christopher Carroll1

JHU

Alan Lujan2

OSU

Mateo Velásquez-Giraldo3

JHU

_____________________________________________________________________________________

Abstract

This paper develops a state-of-the-art computational model of optimal choices for household

spending, investing, and home buying, taking into account the complex interactions between those

and related choices such as mortgage characteristics. Our model can be used to evaluate the extent to

which consumers’ choices are optimal and to suggest strategies for improving their wellbeing

depending on their individual risk aversion and other circumstances. This is the first open source

toolkit that enables easy reproduction of results of this kind and one of few resources

available anywhere including in the private sector that can analyze decisions this complex.

-

Keywords

-

Life-cycle, Portfolio Choice, Housing, Mortgage, Financial

Risk

-

JEL codes

-

1Contact: ccarroll@jhu.edu, Department of Economics, 590 Wyman Hall, Johns Hopkins University,

Baltimore, MD 21218, https://www.econ2.jhu.edu/people/ccarroll, and National Bureau of Economic

Research. 2Contact: lujan.14@osu.edu, Department of Economics, 410 Arps Hall, The Ohio State

University, Columbus, OH 43220, https://economics.osu.edu. 3Contact: mvelasq2@jhu.edu,

Department of Economics, 590 Wyman Hall, Johns Hopkins University, Baltimore, MD 21218,

https://www.econ2.jhu.edu.

1 Introduction

Economists have long sought to use models of mathematically optimal behavior

to try to understand saving and investment decisions over a household’s

life-cycle .

If there were no uncertainty (about, say, investment returns), calculating optimal choices

would not be hard. For example, consumers would want to invest their whole financial

portfolio in whatever asset they knew (in advance) would yield the highest rate of

return.

But in the real world, assets that – on average – yield higher returns (like stocks), also are

much riskier than low-return safe assets (like bank deposits). Aversion to risk is a

perfectly rational motivation, so how much to invest in risky versus safe assets is far

from obvious. Furthermore, there are many other risks (to job, health, to house

prices, and more) that should further temper any rational person’s appetite for risky

investment.

As noted in Carroll (2020) ,

calculating truly optimal behavior in a realistically uncertain world is such a difficult challenge

that only recently has it become feasible to do with a reasonably high degree of realism.

Rational choice models like the one we examined there must account for many important

features of reality, including different types of uncertainty (labor income risk, mortality risk,

and stock market risk), and should allow for reasonable choices of risk aversion, impatience,

and other preferences. They need properly to account for for the path of income over the life

cycle and into retirement, effects of aging and mortality, interest rates and economic growth,

and myriad other factors.

All of this is so difficult that professional financial advisors do not attempt it, relying

instead on rules of thumb and intuition to guide their clients. Indeed, despite the current

excitement about the wonders of artificial intelligence, even online “robo-advisors” do not

incorporate the degree of realism described above. Serious mathematical optimization efforts

have been restricted to the pages of top academic economics journals – and the associated

computer code used to solve the models in those papers has been so impenetrable as to be

unusable.

Carroll (2020) described the first phase of our work sponsored by TFI in building a public,

easy-to-use, open-source software toolkit of the computer code that can solve these kinds of

problems. We showed that our free tools are able easily and quickly to reproduce the results

that have been published in the academic literature.

However, as noted in Carroll (2020), those models of optimal decisionmaking imply that,

given the robust rate of return that risky assets (’stocks’) have earned in the past, most

consumers should invest all of their financial wealth in stocks over most of their

lifetimes.

A tempting interpretation of the discrepancy between the models’ predictions and people’s

actual choices is that most people are just making a mistake in not investing more

in stocks. Another possibility, though, is that the models are still missing some

vitally important (and rational) factor that weighs on people’s actual decisions;

in this case, people might be making rational decisions and the models might be

wrong.

There’s an obvious candidate for the missing factor. For most households homeownership is

the biggest financial decision in their lives. Homeownership should matter for consumers’

choices about how willing they should rationally be to expose themselves to risky financial

assets, for at least two reasons. First, homeownership exposes consumers to housing market

price risk, which should have the effect of reducing their appetite for being exposed

to other kinds of risk. Second, homeownership is associated with certain payment

obligations (not just mortgages, but property taxes, maintenance costs, and so on), which

reduces the flexibility they may have in adjusting their spending in response to income

fluctuations.

These points may seem obvious, but there is a good reason they have not been incorporated

in previous analyses of households’ optimal choice: Taking account of these complexities

greatly increases the computational difficulty of calculating optimal decisions. This technical

report describes results obtained using the latest tools to be added to the Econ-ARK toolkit;

with these tools, it should be much easier for economists, financial planners, and others to

understand the appropriate role of homeownership in modifying investors’ optimal saving and

financial choices.

2 Literature Review

Beginning with Merton (1969) and Samuelson (1969), there is an extensive literature on

portfolio choice over the life-cycle. Cocco, Gomes, and Maenhout (2005) develop a

model of portfolio choice under incomplete markets and with labor income risk

.

Although they are successful in solving a realistically calibrated life-cycle portfolio choice

model, their results imply that most households, and in particular young households with low

liquid wealth should invest all of their assets in the stock market. In reality, however, people

choose a degree of stock market participation and risky share of assets much lower than

what the model proposes would be optimal even for a person with very high risk

aversion .

This gap between observed and actual stock market participation is known as the stock

market participation puzzle, and it remains an open question that is not explained by

state-of-the-art quantitative life-cycle models.

One possible explanation for the stock market participation puzzle could be the absence of

additional forms of asset holding and risk exposure that households face. In particular,

housing has dual properties: Both as an asset and as a source of consumption services .

Housing, however, is different from other assets in that it is illiquid and durable,

providing both future expected wealth (house value of liquidation) as well as shelter

as a consumption service. CHETTY, SÁNDOR, and SZEIDL (2017) empirically

quantify the effect of housing on portfolio choice. Looking at the Survey of Income and

Program Participation (SIPP) panel from 1990 to 2008, the authors establish the

importance of property value and home equity (value minus mortgage debt) on stock

market participation. Importantly, they find that a $10,000 increase in mortgage debt

(holding home equity constant) causes the risky portfolio share to decrease by 0.6

percentage points or $275, which amounts to 3.9% of mean stockholdings in their

data. Importantly for our purposes, they establish the need to distinguish the effects

of home equity and mortgage debt in order to quantify the effect of housing on

portfolios.

This project builds a quantitative model of housing and portfolio choice that can be used to

interpret the empirical findings CHETTY, SÁNDOR, and SZEIDL (2017) in a rich

framework that includes liquid wealth, illiquid housing (size and value), and mortgage debt, in

order to capture the effects of home equity and mortgage debt on portfolio choice. While other

recent work has attempted to shed light on this topic, this model is the first of its kind to

explicitly track home value and mortgage debt separately, allowing them each to evolve with

the decisionmaker’s choices and with economic shocks (say, to house prices). The 2-period

model CHETTY, SÁNDOR, and SZEIDL (2017) develop misses the life-cycle properties of

housing choice and income risk. Additionally, although their empirical findings reveal the

importance of distinguishing home equity and mortgage debt, their model does not

allow these variables to be chosen. Cocco (2005) and Yao and Zhang (2005) do

allow choice of house size but do not distinguish between home equity and mortgage

debt, instead only keeping track of net wealth as the total value of assets minus

liabilities.

2.1 The House-Size Problem

When modeling housing decisions, different assumptions can be made about the “sizes” of

houses that are available for people’s use. The “size” of a house is used to represent a scale of

the different levels of utility that different houses yield, so a “big” house is simply a house that

yields more utility than a “small” house. This section explores how the literature has dealt

with the questions

- What kind of houses can people buy? Is there a finite number of types or a

continuum of sizes?

- Can people change the size of their house without moving to a different house? are

these changes continuous or lumpy? Are they decisions or are they mechanically

tied to other life-cycle characteristics like permanent income?

- Do houses depreciate over time? Can this depreciation be offset?

In Cocco (2005) houses come in a continuum of sizes  and once purchased, the

houses’ sizes can not be changed. Agents can move to a different house of a whatever size they

want every period, but must pay a transaction cost proportional to their current house’s price

to do so. The total cost of moving to a size

and once purchased, the

houses’ sizes can not be changed. Agents can move to a different house of a whatever size they

want every period, but must pay a transaction cost proportional to their current house’s price

to do so. The total cost of moving to a size  house from a size

house from a size  house is

house is

In this model, houses depreciate and agents must (exogenously) pay a

cost

In this model, houses depreciate and agents must (exogenously) pay a

cost  each period to offset depreciation.

each period to offset depreciation.

For Campbell and Cocco (2003), house sizes are exogenously set at the start of the agents’

lives and remain fixed for throughout their duration. The only “moving” that exists in the

model is an exogenous event that can happen with a given probability in any period that

forces the agent to sell his house, liquidate his mortgage and exit the model.There is no

depreciation or associated costs.

Brandsaas (2018) develops a model where agents can rent or own their houses. Houses come

in three fixed sizes; two for owners  and one for renters

and one for renters  . House sizes do

not change, but agents can decide to move from one house size to another in any given period.

Moving into a house entails a moving-cost (additional to the house’s purchase) that is

proportional to the new house’s market value. Houses depreciate at a rate

. House sizes do

not change, but agents can decide to move from one house size to another in any given period.

Moving into a house entails a moving-cost (additional to the house’s purchase) that is

proportional to the new house’s market value. Houses depreciate at a rate  . To offset this,

the owner must (exogenously) pay

. To offset this,

the owner must (exogenously) pay  .

.

In Paz-Pardo (2021), agents can rent or own their houses. Houses come in three sizes: two

for owning and one for renting (as in Brandsaas, 2018), and there is no depreciation. Agents

can switch homes at any time but this entails a monetary cost that is proportional to the

value of the new home. Agents also experience exogenous moving via a Calvo adjustment

probability that forces homeowners to sell their house. Thereafter, households are forced to

spend that period in a rented house.

3 Theoretical Framework

Perhaps the biggest financial decision in a household’s life is buying a house. Houses come in

different sizes (and therefore costs), but they are generally an expensive asset whose value is at

least a few times the household’s yearly income. Young households usually cannot buy their

houses outright, as they start with little to no assets and take time to accumulate enough

resources. They therefore usually rely on mortgages to purchase their houses. These young and

leveraged households might thus be sensitive to stock market risk, causing them to reduce

their stock market participation.

During the repayment period, households’ market resources (or liquid assets) are reduced by

at least the fixed mortgage payment. This has two effects on risky asset choice: 1) It reduces

’market resources’ (current income, plus current non-housing wealth) today, making

households relatively less wealthy, and 2) It reduces market resources in following

periods for any given level of current savings, making households more risk averse due

to the precautionary motive. The fixed nature of mortgage payments has another

important effect: since the household must be sure to have sufficient resources in the

next period to pay their mortgage and the cost of house maintenance, they might

want to save more of their resources in a safe account rather than in the risky stock

market.

Houses are also subject to price fluctuations that depend on local housing market conditions

as well as broader national trends, such as recessions and expansions. The uncertain sale price

of your house, then, constitutes additional uncertainty in future net worth and could thus have

significant implications for portfolio decisions. One way to think about this is to realize that

the owner of a house has an implicit holding of a risky asset, which should motivate them to

want to reduce their exposure to additional risk in another risky asset, the stock

market.

4 Methodology

The new model in our toolkit, which we call ConsPortfolioHousingModel, is an extension of

the model we described in Carroll (2020), ConsPortfolioModel, with the added features of

homeownership such as mortgage payments, house maintenance costs, and housing market price

risk .

4.1 Young Households

The first stage of the model consists of young households making a decision to buy

a house of fixed size. Importantly, young households have little to no assets and

have recently joined the labor market, which means their income is also relatively

small. In order to finance a home, then, young households must choose a house of a

particular value and a corresponding mortgage size. Lenders are assumed to impose some

microprudential conditions such as loan-to-income ratios to ensure that mortgages are

repayable.

4.2 Mortgage payments

Once households choose a house and mortgage, they commit to fixed-rate payments for the

rest of their working life, which is about 30 years. During this time, households have an

implicit holding of a risky asset in their homes (because of their uncertain resale values),

which may lead them to reduce their exposure to other risky assets, such as the stock

market.

4.3 Retired homeowners

Once they reach retirement, households in our model have paid of their mortgage and have

accumulated savings, making them significantly wealthier (where wealth here refers to their

home equity and liquid assets) than young households. During this period, households

experience a risk of house liquidation due to the possibility of being forced to move

out due to poor health or old age. If they are forced to sell, they do so at their

local housing market prices; the value of the house gets transformed into liquid

wealth.

4.4 Retired renters

Retired renters have none of the complexities that come with owning a home, and thus behave

like standard ConsPortfolioModel households. Instead of choosing only consumption,

however, these households choose a level of total expenditures to spend on both consumption

and rental housing. After becoming renters, households remain renters for the rest of their

lives.

5 Results

5.1 Homeownership increases intensive margin of stock market participation

We examine here the behavior of retired households on the cusp of the liquidation of the value

of their house. As usual, we are assuming that the household anticipates some form of

guaranteed pension income (’Social Security’), but expects to finance any other consumption

out of the returns on their assets.

The proportion of liquid assets invested in the stock market is known as the risky portfolio

share, or risky share for short.

Carroll (2020) reviewed the logic of the model without housing. For a person

with no housing wealth and little liquid wealth, the first dollar of investment in the

stock market poses very little risk, so the model implies that the proportion of any

additional wealth that will be invested in the stock market is 100 percent. But as

wealth gets very large, the consumer becomes reluctant to put all of it in the stock

market, because that would be putting more and more of their consumption at

risk .

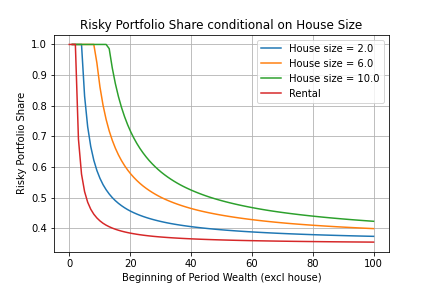

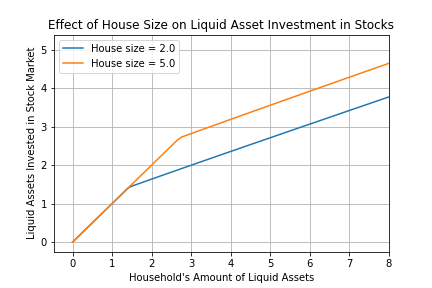

Figure 1 shows how the picture is modified for consumers who, in addition to their liquid

assets, own homes of various sizes.

According to the model, retired households who own their homes and expect to sell them by

next period have a higher risky share than retired households who rent, and their risky share

increases with house size, holding liquid wealth constant.

Clearly, the bigger the house size, the wealthier the agents are in terms of net worth. In the

standard portfolio choice model, wealthier households actually reduce their risky share

to reduce risk in next period’s consumption. In the presence of housing, however,

households still reduce their risk exposure as liquid wealth increases, but at a lower

rate.

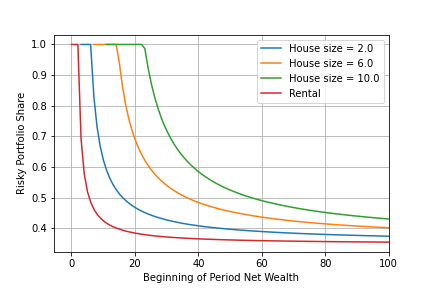

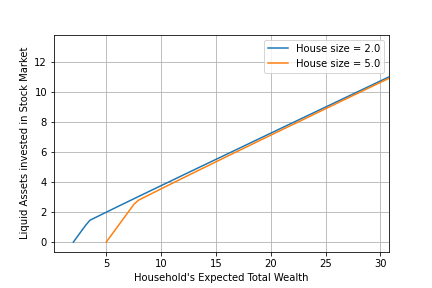

A better comparison is to add the expected value of the house to liquid wealth.

In this way, we compare an agent with  net worth with all liquid wealth

and no home, with an agent with

net worth with all liquid wealth

and no home, with an agent with  net worth, some of which is liquid wealth

net worth, some of which is liquid wealth

, and the rest is the illiquid expected house valuation

, and the rest is the illiquid expected house valuation ![𝔼[Q ]h](PortfolioChoiceWithRiskyHousing12x.svg) , such that

, such that

![w = m + 𝔼[Q ]h](PortfolioChoiceWithRiskyHousing13x.svg) , where

, where  denotes house prices and

denotes house prices and  represents the size of the agent’s

house .

As we see in figure 2, the increase in the risky portfolio share is more significant when

considering home equity as part of net worth. Holding net wealth constant, households whose

wealth is tied up in an illiquid asset have more risk appetite the larger the proportion of home

equity to net wealth is.

represents the size of the agent’s

house .

As we see in figure 2, the increase in the risky portfolio share is more significant when

considering home equity as part of net worth. Holding net wealth constant, households whose

wealth is tied up in an illiquid asset have more risk appetite the larger the proportion of home

equity to net wealth is.

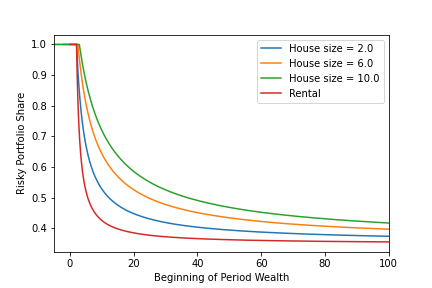

Additionally, an interesting observation is that according to the model retired households

who are about to sell their homes are willing to risk at least the full home equity (expected

value of their homes ![𝔼 [Q ]h](PortfolioChoiceWithRiskyHousing16x.svg) ) for certain when they have low liquidity. In other words, their

risky share is equal to 1 at least up to the point where their liquid wealth is equal to their

home equity. If we shift their liquid wealth leftward by the amount of their expected house

valuation, we see in figure 3 that their risky share starts dropping at about the same point as

it would if they rented a house instead. We can conclude that having a house shifts the

risky share curve rightward by an amount equal to the home equity, but this is

not the only effect. A larger house also reduces the rate at which the risky share

decreases.

) for certain when they have low liquidity. In other words, their

risky share is equal to 1 at least up to the point where their liquid wealth is equal to their

home equity. If we shift their liquid wealth leftward by the amount of their expected house

valuation, we see in figure 3 that their risky share starts dropping at about the same point as

it would if they rented a house instead. We can conclude that having a house shifts the

risky share curve rightward by an amount equal to the home equity, but this is

not the only effect. A larger house also reduces the rate at which the risky share

decreases.

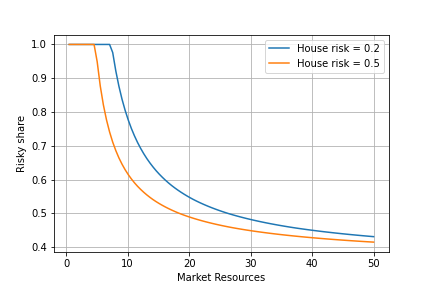

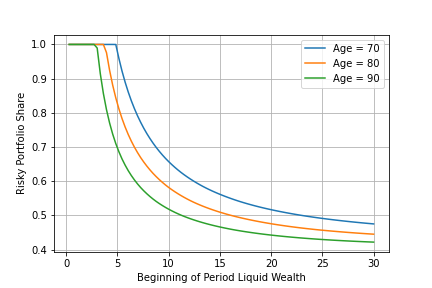

5.2 Increasing house price risk decreases risky share

The volatility of the housing market can have strong implications for the portfolio decisions

of households who own their houses. A higher standard deviation in house prices implies a

larger implicit holding of a risky asset (the house), regardless of house size. For this reason,

households would optimally choose to avoid risk in other risky assets. As we see in figure 4 for

2 households who have a house of equal size, the risky share of a household in a more volatile

market is lower than that of a household in a less volatile market, except at low

levels of market resources. Households that experience high price volatility in the

housing market reduce their exposure to risk elsewhere, leading to lower risky portfolio

shares.

5.3 Larger houses increase households’ absolute risk taking

As mentioned before, a house represents an implicit holding in a risky market that is

otherwise uncorrelated with the stock market. A larger house, however, provides a higher

expected value of house liquidation which also means a higher expected future liquid wealth.

Households with more valuable homes, then, have a higher absolute risk tolerance because

their future housing value constitutes a buffer stock of wealth; thus they invest more

resources in the risky asset market than they would if they had smaller homes.

In figure 5 we see that for an initial level of liquid assets, households of different

house sizes invest the same amount of total assets in the stock market; this is the

region where their risky share is 100%. Past this region, we see that households

with a bigger house (and thus more home equity) are willing to invest a greater

share of their liquid assets than peers with the same amount of liquid assets but less

home equity. This indicates that home equity increases the level of risk appetite for

households.

5.4 House size crowds out investment

However, when comparing households on a total wealth basis, i.e. their liquid assets plus

expected house liquidation, we can see that house size crowds out investment for households

with low liquid wealth. In figure 6, we can consider a household whose house size is

equal to 5 (5 times their yearly net income) and liquid assets are 0, so their total

expected wealth is 5. As this household becomes wealthier, they invest all of their

liquid assets in the stock market (such that their risky share is 100 percent), up to

the point where they start rebalancing their portfolio between the risky and the

safe asset. In this region, they are constrained from investing in the stock market

by their low liquid wealth, as they surely would like to invest more in the market.

This point becomes clearer by comparing the household to an equally wealthy peer

with a smaller house. At the point where the household with house size of 5 has

liquid wealth of 1 (1 times their yearly net income), they are investing less into the

stock market in absolute terms than an equally wealthy household whose house size

is equal to 2 and liquid assets are equal to 4. The total expected wealth of both

these households is 6, but the household with the larger house is investing fewer

assets in the stock market than the household with the smaller house. As their total

wealth increases, however, both households are unconstrained by their house size

and end up investing about the same amount into the stock market in absolute

terms.

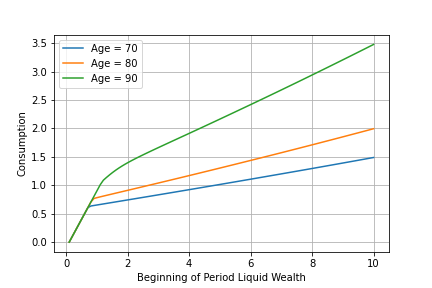

5.5 Optimal Portfolio Choice over the Lifecycle

A result that is consistent with ConsPortfolioModel is that younger households have a higher

risky share of assets than older households, when comparing households of equal house size

and no mortgage debt. Similarly, older households consume more than younger households, as

their consumption horizon gets shorter and the likelihood that they receive a windfall of

wealth from their house liquidation increases.

6 Conclusions

Most people who need advice about how to invest in financial markets are also homeowners.

But until now, even the most sophisticated and realistic analyses of how people should

optimally invest in financial markets have not accounted for the (undeniably important)

ramifications of homeownership for their financial choices.

That’s because constructing a model that correctly tracks all the potential interactions

between homeownership, financial risk, and other kinds of risk is remarkably difficult. This

report describes a free, publicly available open-source software tool that does these complex

calculations. Sponsorship by the Think Forward Initiative has allowed us to add this tool to

the free, open-source, Econ-ARK toolkit, thus making it available to financial institutions,

financial planners, robo-advisors, academics, and anyone else who might be interested in a

rigorous analysis of these questions.

Despite their combinatorial complexity, the answers that come from the model make

intuitive sense. A first conclusion is that greater uncertainty about future house prices should

make you less willing to invest in the stock market. In other words, a homeowner who

lives in a place with wild house-price swings will find it best to have less exposure

to other kinds of risk (like stock market risk) than someone with circumstances

that are otherwise similar, but who lives in a place where house prices are more

stable.

Another conclusion might seem to push in the other direction, but really does not:

Among homeowners whose mortgage is paid off, for a given level of nonhousing net

worth (say, $200K of financial assets net of mortgage debt), a person whose house is

more valuable should invest more in risky financial asset. The reason is simple: For

a given amount of liquid assets, the person with a bigger house is richer, and a

richer person will want to have more money (in absolute terms) invested in the stock

market).

The final point is that the existence of homeownership does not reverse one of the more

surprising implications of the baseline model without homeownership: The richer you are, the

lower is the optimal share of your portfolio in risky assets. This implication of the model does

not match the available data well. The conclusion is easy to reverse by introducing a bequest

motive in which bequests are a luxury good; but how exactly such a motive should be

constructed is by no means a settled question, either among financial planners or

among academic researchers. It is a topic we hope to address in future releases of our

toolkit.

Appendices

A The base model

At date 0, the household finances the purchase of a house with a mortgage loan. Given

cash-on-hand at date 0  , which may come from previous savings or bequests, the

household simultaneously chooses a house size (among a set of discrete house sizes)

and a mortgage loan that meets the down-payment or Loan-to-Value requirement

, which may come from previous savings or bequests, the

household simultaneously chooses a house size (among a set of discrete house sizes)

and a mortgage loan that meets the down-payment or Loan-to-Value requirement

, where

, where  is the proportional down-payment,

is the proportional down-payment,  is the unit-price of

housing, and

is the unit-price of

housing, and  is the chosen house size. An additional mortgage origination requirement

observed in the literature is the Loan-to-Income ratio

is the chosen house size. An additional mortgage origination requirement

observed in the literature is the Loan-to-Income ratio  , which reflects initial

mortgage affordability (Campbell and Cocco (2015)). Coincidentally, the household leaves

some cash-on-hand

, which reflects initial

mortgage affordability (Campbell and Cocco (2015)). Coincidentally, the household leaves

some cash-on-hand  to start next period with some liquidity.

to start next period with some liquidity.

![V0 (M0, P1) = Dm1a,xH1𝔼t [V1 (M1, H1,D1, P1 )]

s.t.

Q0H1+ M1 = M0 + D1

H ∈ ℍ = {h ,⋅⋅⋅,h }

1 1 n

D1 ≤ (1 − d)Q0H1 (LTV )

D1 ≤ λP1 (LTI )](PortfolioChoiceWithRiskyHousing24x.svg) | (1) |

A.1 Fixed-Rate Mortgage payments

When a household chooses a house size and mortgage loan, they also commit to a fixed

payment amount and a loan duration of, for example, 30 years. To calculate the fixed rate

mortgage payment ( ), we can start with the amount owed at the beginning of each

period

), we can start with the amount owed at the beginning of each

period  and subtract a fixed payment, which is then multiplied by a fixed mortgage

interest rate

and subtract a fixed payment, which is then multiplied by a fixed mortgage

interest rate  . The limiting condition that ensures repayment at time

. The limiting condition that ensures repayment at time  is

is  ,

which leads to

,

which leads to  as shown below:

as shown below:

| (2) |

where  . Setting

. Setting  as a repayment requirement, the fixed rate

mortgage payment is

as a repayment requirement, the fixed rate

mortgage payment is

| (3) |

The household is allowed to pay more than its required mortgage payment, which in this

model leads to a decrease in the future minimum required payment  to maintain

the mortgage duration. If the household continually pays more than the minimum

payment,

to maintain

the mortgage duration. If the household continually pays more than the minimum

payment,  becomes

becomes  when the mortgage debt is fully paid off. This flexibility

allows for the fixed rate mortgage payment to depend only on current mortgage debt

when the mortgage debt is fully paid off. This flexibility

allows for the fixed rate mortgage payment to depend only on current mortgage debt

and time to mortgage maturity, which is tracked by the age of the household

and time to mortgage maturity, which is tracked by the age of the household

.

.

A.2 The Investor’s problem in the presence of housing risk

A.2.1 Investing before Retirement

A working household begins period  with cash-on-hand

with cash-on-hand  , housing size

, housing size  ,

mortgage debt

,

mortgage debt  , and permanent income

, and permanent income  . It must then choose a level of consumption

. It must then choose a level of consumption

, mortgage payment

, mortgage payment  , and savings

, and savings  of which a fraction

of which a fraction  is invested into a risky

asset and the rest into a safe asset.

is invested into a risky

asset and the rest into a safe asset.

The mortgage payment must be at least the fixed rate mortgage payment  in

order to ensure payoff within an expected maturity of

in

order to ensure payoff within an expected maturity of  years.

years.

Although the model does not allow for explicit choices over housing adjustments, the

household must nevertheless pay maintenance and upkeep costs due to housing depreciation at

a cost of  . Additionally, the household must also exogenously expand or contract their

housing size given a life-cycle path of housing size

. Additionally, the household must also exogenously expand or contract their

housing size given a life-cycle path of housing size  . This parameter is intended to

represent the observed path of the housing size component of portfolio compositions over the

life-cycle.

. This parameter is intended to

represent the observed path of the housing size component of portfolio compositions over the

life-cycle.

![Vt (Mt, Ht, Dt,Pt ) = mAatx,It,ςtu(Ct,Ht ) + β 𝔼t[Vt+1(Mt+1, Ht+1, Dt+1,Pt+1)]

s.t.

At = Mt − Ct − It

At ≥ 0

It ≥ FRMt + [Ht+1 − (1 − δ)Ht]Q0

Pt+1 = Γ t+1Pt

Yt+1 = 𝜃t+1Pt+1

M = Y + A (ςR + (1 − ς )R)

t+1 t+1 t t t+1 t

Ht+1 = Γ Ht+1Ht

Dt+1 = RD (Dt − It)](PortfolioChoiceWithRiskyHousing53x.svg) | (4) |

A.2.2 Investing after Retirement

Households deterministically retire at age  , and begin to experience exogenous risk of

housing liquidation. By this time, the household has finished paying their mortgage debt, and

so we lose the

, and begin to experience exogenous risk of

housing liquidation. By this time, the household has finished paying their mortgage debt, and

so we lose the  state variable. If the household is exogenously forced to liquidate

their house, they receive their home equity at the beginning of next period and

become renters until death. The problem of a household which faces housing risk

is

state variable. If the household is exogenously forced to liquidate

their house, they receive their home equity at the beginning of next period and

become renters until death. The problem of a household which faces housing risk

is

![VHt (Mt, Ht, Pt) = max u (Ct,Ht) + βst 𝔼t[VHt+1(Mt+1, Ht+1,Pt+1)]

Ct,At,ςt

+ β(1 − st)𝔼t[VR (M R ,Pt+1)]

t+1 t+1

s.t.

At = Mt − Ct − It, At ≥ 0

It ≥ [Ht+1 − (1 − δ)Ht]Q0

Pt+1 = Γ t+1Pt

Yt+1 = 𝜃t+1Pt+1

Mt+1 = Yt+1 + At(ςtRt+1 + (1 − ςt)R)

R

M t+1 = Mt+1 + Qt+1Ht+1

H = Γ H H

t+1 t+1 t](PortfolioChoiceWithRiskyHousing56x.svg) | (5) |

The renter’s problem then becomes a simple portfolio problem where the household

additionally pays for rental housing.

![VR (M ,P ) = max u (C ,HR ) + β 𝔼 [VR (M ,P )]

t t t Ct,HRt ,At,ςt t t t t+1 t+1 t+1

s.t.

R R

At = Mt − Ct − H t , Ct,H t ,At ≥ 0

M = Y + A (ςR + (1 − ς )R)

t+1 t+1 t t t+1 t

Pt+1 = Γ t+1Pt

Yt+1 = 𝜃t+1Pt+1](PortfolioChoiceWithRiskyHousing57x.svg) | (6) |

B Normalization

A useful strategy to facilitate finding the solution of these types of problems is normalization

by permanent income. Throughout this section we assume

| (7) |

which is a Cobb-Douglas function nested inside a CRRA utility function. The model

parameter  determines the relative preference between non-durable consumption and

housing size. In a simple rental housing problem, it also determines directly the rental housing

share of total expenditures, as we’ll see below.

determines the relative preference between non-durable consumption and

housing size. In a simple rental housing problem, it also determines directly the rental housing

share of total expenditures, as we’ll see below.

B.1 Rental Housing in the Utility

A renter pays for rental housing every period until death. Rental housing enters the utility as

a non-durable expenditure and, like consumption, it has no impact on the continuation

value. Using the utility function described above, and representing non-durable

total expenditures as  , utility maximization implies that

, utility maximization implies that  ,

,

, and

, and  . Substituting these results into the utility function, it

becomes:

. Substituting these results into the utility function, it

becomes:

| (8) |

Thus, we can represent the problem of total expenditures between consumption and rental

housing as  , where

, where  is a CRRA utility function with

is a CRRA utility function with  coefficient.

coefficient.

B.2 The Retired Renter’s last period of life

In the last period of life, a renter has no need to save and thus has to decide to

spend all of his cash-on-hand ( ) between non-durable consumption and rental

housing.

) between non-durable consumption and rental

housing.

| (9) |

Again, utility maximization implies that  and

and  . Substituting into

the previous equation we obtain:

. Substituting into

the previous equation we obtain:

| (10) |

where  . We can now normalize by permanent income

. We can now normalize by permanent income  such that

lowercase variables are

such that

lowercase variables are  . Substituting

. Substituting  , the expression

becomes

, the expression

becomes

| (11) |

If we define a normalized equation as  then the original problem can be

rewritten as

then the original problem can be

rewritten as

| (12) |

B.3 The Retired Renter’s second-to-last period

We can now consider the second-to-last period, although the same analysis will apply

recursively to any period with a non-zero continuation value. Normalizing as above, where

, we obtain

, we obtain

![VRT− 1(MT −1,PT− 1) = maxR u (CT −1,HT − 1) + β 𝔼t[VRT (MT ,PT )]

CT−1,HT−1,ςT−1

= max A˜u (x P ) + β 𝔼 [P1− ρΓ 1−ρ˜AvR (m )]

xT−1,ςT−1 T −1 T− 1 t T− 1 T T T

{ }

= A˜P T1−− ρ1 max u(xT− 1) + β 𝔼t[Γ 1T−ρvRT (mT )]

xT−1,ςT−1](PortfolioChoiceWithRiskyHousing81x.svg) | (13) |

We can again define the normalized value function as  and re-write

the problem as

and re-write

the problem as

![vRT−1(mT −1) = max u(xT −1) + β 𝔼t [Γ 1−T ρvRT(mT )]

xT−1,ςT−1](PortfolioChoiceWithRiskyHousing83x.svg) | (14) |

The generalized renter’s problem with non-zero continuation value then simplifies to a

simple consumption and portfolio choice problem with additionally defined control variables as

presented below.

![R 1−ρ R

vt (mt ) = maxxt,ςt u(xt) + β 𝔼t[Γ t+1 vt+1 (mt+1)]

s.t.

at = mt − xt, xt,at ≥ 0

ct = (1 − α)xt,

ht = αxt

mt+1 = 𝜃t+1 + at(ςtRt+1 + (1 − ςt)R )∕Γ t+1](PortfolioChoiceWithRiskyHousing84x.svg) | (15) |

B.4 The Retired Homeowner’s last period of life

We assume homeowners deterministically become renters before their last period of

life.

B.5 The Retired Homeowner’s second-to-last period of life

In their second-to-last period of life, a homeowner will become a renter in the next period with

certainty. Note that by this stage of life the household has no outstanding mortgage debt.

Their problem is

![VHT−1(MT −1,HT − 1,PT −1) = max u(CT− 1,HT −1) + β 𝔼t[VRT(M RT ,PT)]

CT−1,AT−1,ςT−1

s.t.

CT −1 + AT −1 = MT −1 − [Γ HT−1 − (1 − δ )]Q0HT −1, CT −1,AT −1 ≥ 0

R H

M T = YT + AT− 1(ςT− 1RT + (1 − ςT−1)R ) + QT Γ T−1HT −1

PT = Γ TPT− 1

YT = 𝜃T PT](PortfolioChoiceWithRiskyHousing85x.svg) | (16) |

A similar normalization procedure as above yields the following equivalent problem

![vH (m ,h ) = max u(c ,h ) + A˜β 𝔼[Γ 1−ρvR (mR )]

T−1 T− 1 T−1 cT−1,aT− 1,ςT− 1 T−1 T −1 T T T

s.t.

H

cT −1 + aT−1 = mT − 1 − [ΓT− 1 − (1 − δ)]Q0hT −1, cT− 1,aT−1 ≥ 0

mR = 𝜃T + aT −1(ςT −1RT + (1 − ςT−1)R )∕Γ T + QT Γ H hT− 1∕ Γ T

T T−1](PortfolioChoiceWithRiskyHousing86x.svg) | (17) |

B.6 The Retired Homeowner’s general problem

A retired homeowner has no mortgage debt or payments, but does experience house

liquidation and house price risk. With probability  , the homeowner will be forced to

sell their house and become a renter next period, in which case they obtain the value of their

home as a liquid asset.

, the homeowner will be forced to

sell their house and become a renter next period, in which case they obtain the value of their

home as a liquid asset.

![VH (M ,H ,P ) = max u (C ,H ) + βs 𝔼 [VH (M ,H ,P )]

t t t t Ct,At,ςt t t t t t+1 t+1 t+1 t+1

R R

+ β(1 − st)𝔼t[Vt+1(M t+1,Pt+1)]

s.t.

Ct + At = Mt − [Ht+1 − (1 − δ)Ht ]Q0, Ct, At ≥ 0

Mt+1 = Yt+1 + At(ςtRt+1 + (1 − ςt)R)

R

M t+1 = Mt+1 + Qt+1Ht+1

H

Ht+1 = Γt+1Ht

Pt+1 = Γ t+1Pt

Yt+1 = 𝜃t+1Pt+1](PortfolioChoiceWithRiskyHousing88x.svg) | (18) |

The normalized version of their problem is

![H [ 1−ρ ( H ˜ R R ) ]

vt (mt,ht) = mcat,xat,ςtu(ct,ht) + β 𝔼t Γt+1 stvt+1(mt+1,ht+1) + (1 − st)Av t+1(m t+1 )

s.t.

H

ct + at = mt − [Γ t+1 − (1 − δ)]Q0ht, ct,at ≥ 0

m = 𝜃 + a (ςR + (1 − ς )R)∕Γ , 0 ≤ ς ≤ 1

t+1 t+1 t t t+1 t t+1 t

ht+1 = Γ Ht+1ht ∕Γ t+1

mRt+1 = mt+1 + Qt+1ht+1](PortfolioChoiceWithRiskyHousing89x.svg) | (19) |

B.7 The Working Homeowner that has mortgage debt

B.8 The borrowing constraint

Every household arrives at the last period of the model as a retired renter. Because they will

die with certainty by the end of the period, there is a strict no-borrowing constraint imposed

for these households ( ). This implies that the minimum allowable level of market

resources is also

). This implies that the minimum allowable level of market

resources is also  . If the household arrived to the last period with a negative

level of market resources, it would have to consume a negative amount, yielding

. If the household arrived to the last period with a negative

level of market resources, it would have to consume a negative amount, yielding  utility.

utility.

This strict borrowing constraint in the last period leads to a self imposed borrowing

constraint in the second to last period, as the precautionary savings motive induces households

to meet a minimum allowable level of market resources next period in order to avoid  utility.

utility.

For the retired renter household, that means

| (20) |

Because renting households have no collateral (a home), we can assume an artificial

no-borrowing constraint. The minimum allowable level of market resources next period is met

as long as  , which is true by construction. The no-borrowing constraint, in turn,

induces a minimum allowable level of market resources in the second to last period as

, which is true by construction. The no-borrowing constraint, in turn,

induces a minimum allowable level of market resources in the second to last period as

. Recursively, we can continue to assume a no-borrowing constraint for every period

imposed on the retired renter household, which implies

. Recursively, we can continue to assume a no-borrowing constraint for every period

imposed on the retired renter household, which implies  and

and  for all

for all  during retirement.

during retirement.

The retired homeowner in their second to last period will become a renter with certainty

by the next period, at which point they receive the cash value of their liquidated

house.

| (21) |

which implies a natural minimum allowable level of market resources for homeowners

of

| (22) |

The last period market resources for homeowners is ruled by the transition equation

| (23) |

Given a household’s decision on asset level  , the lowest possible realization of next

period market resources occurs when the household receives the lowest possible return, along

with the lowest realizations of income shocks next period. For each

, the lowest possible realization of next

period market resources occurs when the household receives the lowest possible return, along

with the lowest realizations of income shocks next period. For each  , then, there is an

upper bound on the risky share

, then, there is an

upper bound on the risky share  such that the minimum allowable level of future market

resources is met.

such that the minimum allowable level of future market

resources is met.

| (24) |

which implies a natural risky share constraint of

| (25) |

The natural borrowing constraint, then, occurs when the implied natural risky share

constraint is  , which is

, which is

| (26) |

The minimum allowable level of market resources constraint is once again derived from the

precautionary motive  , which results in

, which results in

![H

mT −1(hT− 1) = aT −1(hT−1) + [ΓT−1 − (1 − δ)]Q0hT −1.](PortfolioChoiceWithRiskyHousing111x.svg) | (27) |

An important issue arises in the third-to-last period. Households who will become renters

next period only have to meet the minimum allowable level of market resources for rental

households next period  or equivalently

or equivalently  . Households

who will remain homeowners instead have to meet the minimum allowable level of market

resources for home-owning households next period (determined above). However, unlike in

the second-to-last period, households in the third-to-last period do not know what

type they will be in the next period, so they must meet both constraints, and thus

must meet the stricter constraint. The effective minimum allowable level of market

resources for the second to-last-period

. Households

who will remain homeowners instead have to meet the minimum allowable level of market

resources for home-owning households next period (determined above). However, unlike in

the second-to-last period, households in the third-to-last period do not know what

type they will be in the next period, so they must meet both constraints, and thus

must meet the stricter constraint. The effective minimum allowable level of market

resources for the second to-last-period  and recursively for periods before it

is:

and recursively for periods before it

is:

![m-∗t(ht) = max {at(ht) + [Γ Ht − (1 − δ)]Q0ht,− Qtht}](PortfolioChoiceWithRiskyHousing115x.svg) | (28) |

and the general natural borrowing constraint for period  and recursively for every

period before it is

and recursively for every

period before it is

| (29) |

C Backsolving the problem

The overall return on the consumer’s portfolio is

| (30) |

The first order condition with respect to  is

is

![[ −ρ ( ) ]

u ′1(ct,ht) = β 𝔼t Γ t+1Rt+1 st∂mvHt+1(mt+1, ht+1 ) + (1 − st) ˜A∂mvRt+1(mRt+1)](PortfolioChoiceWithRiskyHousing120x.svg) | (31) |

The first order condition with respect to  is

is

![[ ( )]

0 = β 𝔼 Γ −ρ(R − R) s ∂ vH (m ,h ) + (1 − s ) ˜A ∂ vR (mR ) a

t t+1 t+1 t m t+1 t+1 t+1 t m t+1 t+1 t](PortfolioChoiceWithRiskyHousing122x.svg) | (32) |

A useful function to define is

![[ 1−ρ ( H R R ) ]

𝔳t(at,ςt) = β 𝔼t Γt+1 stvt+1 (mt+1, ht+1) + (1 − st)A˜v t+1(m t+1)](PortfolioChoiceWithRiskyHousing123x.svg) | (33) |

with first order conditions

which implies first order conditions for the problem

We can define the problem

| (38) |

which leads to solution

| (39) |

we can solve for consumption function as

| (40) |

Similarly, as before, the Envelope condition is

| (41) |

D Portfolio Choice after retirement

D.1 The solution of risky share

Let  be log-normally distributed such that

be log-normally distributed such that  , then it is true

that

, then it is true

that

![𝔼 [R ] = er+σ2r∕2 and Var [R ] = (eσ2r − 1)e2r+ σr2

t t+1 t t+1](PortfolioChoiceWithRiskyHousing132x.svg) | (42) |

Thus, if we want to produce a log-normal distribution with mean  and variance

and variance  , we

can use a normal distribution with

, we

can use a normal distribution with

| (43) |

According to Campbell and Viceira, the optimal share of stocks in financial wealth for an

agent that is not facing income uncertainty is

| (44) |

Using the above relations, we know that

| (45) |

D.2 Exogenous Risky Share

Given the solution of portfolio choice after retirement, if we want to target a particular risky

share  (for example, one that fits the observed data on portfolio choice after retirement), we

can back out the agent’s beliefs on the risky asset return that would rationalize such an

(for example, one that fits the observed data on portfolio choice after retirement), we

can back out the agent’s beliefs on the risky asset return that would rationalize such an  .

Assuming we know an agent’s financial wealth (human and non-human), we can fix

.

Assuming we know an agent’s financial wealth (human and non-human), we can fix  to find an ex-ante belief on the variance of the risky distribution that rationalizes an

exogenous risky share

to find an ex-ante belief on the variance of the risky distribution that rationalizes an

exogenous risky share  as

as

| (46) |

Fixing  and finding a

and finding a  that rationalizes an exogenous risky share

that rationalizes an exogenous risky share  has no analytical solution, although a numerical solution might exist under some

conditions.

has no analytical solution, although a numerical solution might exist under some

conditions.

Of course, if instead we fix  or

or  , we can obtain rationalized

beliefs as

, we can obtain rationalized

beliefs as

| (47) |

and

| (48) |

It’s important to note that these beliefs will result in different risky distribution parameters

than those that pegged the log-normal distribution parameter.

E The Portfolio Choice Problem for Rental Households

Households that do not own and instead rent their homes have to decide how much to

consume, how much to spend on rent, and how much to save. Their normalized problem can

be stated as:

![[ ]

wt(mt) = max u(ct,ht) + β 𝔼t Γ 1−t+1ρwt+1(mt+1 )

{at,ht,ςt}

s.t.

at = mt − ct − ht

Rt+1(ςt) = R + (Rt+1 − R)ςt

mt+1 = atRt+1 (ςt)∕Γ t+1 + 𝜃t+1](PortfolioChoiceWithRiskyHousing150x.svg) | (49) |

Consider the problem of a consumer that has  to spend on consumption and housing.

Their problem is

to spend on consumption and housing.

Their problem is

| (50) |

Given the functional form of utility we are using (CRRA with paramter  ), the well known

solution to this simple problem is

), the well known

solution to this simple problem is  and

and  . Restating the problem in

terms of

. Restating the problem in

terms of  , we obtain:

, we obtain:

| (51) |

where  . Because both consumption and housing are non-durable in

the case of a rental household, the consumer can first decide how much to spend on both

goods (

. Because both consumption and housing are non-durable in

the case of a rental household, the consumer can first decide how much to spend on both

goods ( ) and then decide how much to spend on each of the goods without changing the

problem. A further step to simplify the problem is to use iterated expectations to split up the

problem into subperiods. We can define

) and then decide how much to spend on each of the goods without changing the

problem. A further step to simplify the problem is to use iterated expectations to split up the

problem into subperiods. We can define

![[ 1−ρ ]

wt (bt+1) = 𝔼t Γt+1wt+1(mt+1 )

where

mt+1 = bt+1∕Γ t+1 + 𝜃t+1](PortfolioChoiceWithRiskyHousing160x.svg) | (52) |

Now, we can rewrite our original problem as

![wt(mt ) = m{aatx,ςt}u(xt) + β 𝔼t [wt(bt+1)]

s.t.

at = mt − xt

R (ς ) = R + (R − R )ς

t+1 t t+1 t

bt+1 = atRt+1(ςt)](PortfolioChoiceWithRiskyHousing161x.svg) | (53) |

which embeds the simple subproblem and our defined iterated expectation.

We can rewrite the problem as

![wt (mt) = m{aaxt,ςt}u (mt − at) + β 𝔼t [wt (at(R + (Rt+1 − R )ςt))]](PortfolioChoiceWithRiskyHousing162x.svg) | (54) |

First order condition with respect to  provides the Euler equation

provides the Euler equation

![u′(x ) = β 𝔼 [w ′(b )R (ς )]

t t t t+1 t+1 t](PortfolioChoiceWithRiskyHousing164x.svg) | (55) |

and the first order condition with respect to  is

is

![′

β 𝔼t [wt(bt+1)at(Rt+1 − R )] = 0](PortfolioChoiceWithRiskyHousing166x.svg) | (56) |

The envelope condition is given by

| (57) |

And finally,

![w ′(bt+1) = 𝔼t [Γ 1−ρw ′ (mt+1 )∕Γ t+1] = 𝔼t [Γ −ρ w ′ (mt+1 )]

t t+1 t+1 t+1 t+1](PortfolioChoiceWithRiskyHousing168x.svg) | (58) |

F The portfolio problem of a homeowner with no mortgage

A homeowner with no mortgage debt is allowed to invest more on their house to increase its

size (or they can let it depreciate). In doing so, they choose home investment, consumption,

and savings. Their problem is summarized as follows:

![[ 1−ρ( w )]

vt(mt, ht−1) = maat,xςt,itu(ct,ht) + β 𝔼t Γt+1 (1 − 𝜗 )vt+1(mt+1, ht+1) + 𝜗wt+1(m t+1)

s.t.

ht = (1 − δ)ht−1 + it∕ ϙ0

ht+1 = ht∕ Γ t+1

at = mt − ct − it

Rt+1(ςt) = R + (Rt+1 − R)ςt

mt+1 = atRt+1 (ςt)∕Γ t+1 + 𝜃t+1

mw = mt+1 + ϙ ht+1

t+1 t+1](PortfolioChoiceWithRiskyHousing169x.svg) | (59) |

To facilitate the solution method, we can split the above problem into different

subperiods.

In the first subperiod, the household arrives with cash on hand and their previous housing

size. They then pick their current size by investing  where housing costs are

where housing costs are  . After

investing, they are left with net cash on hand after housing costs, and a new housing

size.

. After

investing, they are left with net cash on hand after housing costs, and a new housing

size.

| (60) |

In the second subperiod, the household arrives with net cash on hand and their current

housing size. This subperiod is a standard portfolio choice problem, indexed by their house

size. The agent must then choose a level of savings  and the proportion of their savings

that will go into the risky asset

and the proportion of their savings

that will go into the risky asset  versus the safe asset

versus the safe asset  .

.

![[ ]

˜𝔳t(nt,ht) = max u (ct,ht) + β 𝔼t `˜𝔳t(bt+1, ht)

{at,ςt}

at = nt − ct

R (ς) = R + (R − R)ς

t+1 t t+1 t

bt+1 = atRt+1(ςt)](PortfolioChoiceWithRiskyHousing176x.svg) | (61) |

Finally in the last subperiod, the household’s uncertainty is realized. Simultaneously, they

observe their permanent and transitory income shocks, whether they will become renters in

the next period (function  with probability

with probability  ), and if they do become renters, the

liquidation price of their house per unit of housing.

), and if they do become renters, the

liquidation price of their house per unit of housing.

![`˜ [ 1−ρ( w )]

𝔳t(bt+1,ht) = 𝔼t Γ t+1 (1 − 𝜗)vt+1(mt+1, ht+1) + 𝜗wt+1 (m t+1 )

where

ht+1 = ht∕Γ t+1

mt+1 = bt+1 ∕Γ t+1 + 𝜃t+1

w

m t+1 = mt+1 + ht+1ϙt+1](PortfolioChoiceWithRiskyHousing179x.svg) | (62) |

F.1 First order conditions: Choosing home investment

The problem is

| (63) |

The first order condition with respect to  is

is

| (64) |

which equalizes the marginal benefit of additional net cash-on-hand (cash-on-hand net of

home investment) with the marginal cost of a larger house. The envelope conditions

are

| (65) |

F.2 First order conditions: Choosing consumption and portfolio investment

Once again, let’s reduce the problem to 1 line.

![[ ]

˜𝔳 (n ,h ) = max u(n − a ,h) + β 𝔼 `˜𝔳(a (R + (R − R)ς),h )

t t t {at,ςt} t t t t t t t+1 t t](PortfolioChoiceWithRiskyHousing184x.svg) | (66) |

Notice that  passes through this problem unaltered. Indeed, in this subproblem, the

house size indexes the portfolio choice (and may affect marginal utility) but does not need

further addressing beyond a simple portfolio choice model.

passes through this problem unaltered. Indeed, in this subproblem, the

house size indexes the portfolio choice (and may affect marginal utility) but does not need

further addressing beyond a simple portfolio choice model.

The first order condition with respect to  is

is

![[ ]

uc(c,h ) = β 𝔼 `˜𝔳b(b ,h )R (ς )

t t t t t+1 t t+1 t](PortfolioChoiceWithRiskyHousing187x.svg) | (67) |

The first order condition with respect to  is

is

![[ b ]

β 𝔼t `˜𝔳t(bt+1,ht)at(Rt+1 − R) = 0](PortfolioChoiceWithRiskyHousing189x.svg) | (68) |

Finally, the envelope conditions are

![˜𝔳nt (nt,ht) = uc(ct,ht)

h h [ h ]

˜𝔳 t(nt,ht) = u (ct,ht) + β 𝔼t `˜𝔳t(bt+1,ht)](PortfolioChoiceWithRiskyHousing190x.svg) | (69) |

The second envelope condition is due to the nature of the  pass-through.

pass-through.

F.3 Envelope conditions: Uncertainty is realized

The last subperiod is harder to re-write in one line, but because there is no maximization it is

straight forward to calculate the derivatives.

![`˜b [ −ρ ( m m w )]

𝔳t(bt+1,ht) = 𝔼t [Γt+1((1 − 𝜗)vt+1(mt+1, ht+1) + 𝜗w t+1(m t+1) )]

`˜𝔳h(bt+1,ht) = 𝔼t Γ −ρ (1 − 𝜗)vh (mt+1, ht+1) + 𝜗wm (mw )ϙ

t t+1 t+1 t+1 t+1 t+1](PortfolioChoiceWithRiskyHousing192x.svg) | (70) |

G Solving the homeowner with mortgage problem

![v (m ,h ,d ) = max u(c ,h ) + β 𝔼 [Γ 1−ρv (m ,h ,d )]

t t t t−1 at,ςt,it t t t t+1 t+1 t+1 t+1 t+1

s.t.

d = d + (1 − δ)h − i

t t−1 t t

at = mt − ct − it

Rt+1 (ςt) = R + (Rt+1 − R )ςt

mt+1 = atRt+1(ςt)∕Γ t+1 + 𝜃t+1

h = h ∕Γ

t+1 t t+1

mwt+1 = mt+1 + ϙt+1ht+1](PortfolioChoiceWithRiskyHousing193x.svg) | (71) |

Can also be split up into subparts

| (72) |

![[ ]

`

˜𝔳t(nt,ht,dt) = {maat,xςt}u (ct,ht) + β 𝔼t ˜𝔳t(bt+1, ht,dt)

at = nt − ct

Rt+1(ςt) = R + (Rt+1 − R)ςt

b = a R (ς )

t+1 t t+1 t](PortfolioChoiceWithRiskyHousing195x.svg) | (73) |

![`˜ [ 1−ρ ]

𝔳t(bt+1,ht,dt) = 𝔼t Γt+1vt+1(mt+1,ht+1,dt+1)

where

ht+1 = ht∕Γ t+1

dt+1 = dtRD ∕Γ t+1

mt+1 = bt+1∕Γ t+1 + 𝜃t+1

mw = m + h ϙ

t+1 t+1 t+1 t+1](PortfolioChoiceWithRiskyHousing196x.svg) | (74) |

References

Brandsaas, Eirik (2018): “Household Stock Market Participation: The Role of

Homeownership,” SSRN Electronic Journal.

Campbell, John Y., and João F. Cocco (2003): “Household risk

management and optimal mortgage choice,” Quarterly Journal of Economics, 118(4),

1449–1494.

__________ (2015): “A Model of Mortgage Default,” Journal of Finance, 70(4),

1495–1554.

Carroll, Christopher (2020): “Optimal Financial

Investments Over the Life Cycle,” Think Forward Initiative,

(https://www.thinkforwardinitiative.com/stories/optimal-financial-investments-over-the-life-cycle).

CHETTY, RAJ, LÁSZLÓ SÁNDOR, and ADAM SZEIDL (2017): “The

Effect of Housing on Portfolio Choice,” The Journal of Finance, 72(3), 1171–1212.

Cocco, João F. (2005): “Portfolio choice in the presence of housing,” Review of

Financial Studies, 18(2), 535–567.

Cocco, João F., F. J. Gomes, and Pascal J. Maenhout (2005):

“Consumption and portfolio choice over the life cycle,” Review of Financial Studies,

18(2), 491–533.

Gomes, Francisco (2020): “Portfolio Choice over the Life Cycle: A Survey,”

Annual Review of Financial Economics, 12(1), 277–304.

Gomes, Francisco, and Alexander Michaelides (2005): “Optimal life-cycle

asset allocation: Understanding the empirical evidence,” Journal of Finance, 60(2),

869–904.

Merton, Robert C. (1969): “Lifetime Portfolio Selection under Uncertainty: The

Continuous-Time Case,” The Review of Economics and Statistics, 51(3), 247.

Paz-Pardo, Gonzalo (2021): “Homeownership and Portfolio Choice over the

Generations,” Ssrn, pp. 1–87.

Samuelson, Paul A. (1969): “Lifetime Portfolio Selection By Dynamic Stochastic

Programming,” The Review of Economics and Statistics, 51(3), 239.

Yao, Rui, and Harold H. Zhang (2005): “Optimal consumption and portfolio

choices with risky housing and borrowing constraints,” Review of Financial Studies,

18(1), 197–239.

![[ ( )]

𝔳a = β 𝔼t Γ − ρRt+1 st∂mvH (mt+1, ht+1) + (1 − st)A˜∂mvR (mR ) (34)

t [ t+1 (t+1 t+1 t+1 ) ]

𝔳 ς = β 𝔼 Γ − ρ(R − R ) s ∂ vH (m ,h ) + (1 − s )A ˜∂ vR (mR ) a(35)

t t t+1 t+1 t m t+1 t+1 t+1 t m t+1 t+1 t](PortfolioChoiceWithRiskyHousing124x.svg)