Benhabib, Bisin, and Luo (2019) — Ballpark Entry¶

Paper: Jess Benhabib, Alberto Bisin, and Mi Luo, “Wealth Distribution and Social Mobility in the US: A Quantitative Approach,” American Economic Review, 109(5), 1623–1647, 2019. DOI: 10.1257/aer.20151684

Original ballpark author: Ashish Kumar (March 2024)

Updated by: llorracc — 2026-01-27; 2026-04-27 (post-paper-and-appendix review; see bellman-excerpt.md Open Issue #10)

Pitch — why this paper is in the ballpark:

What the paper uniquely does. The paper jointly estimates three structural channels for the U.S. wealth distribution — skewed lifecycle earnings, wealth-dependent bequest motives, and heterogeneous stochastic returns — by simultaneously targeting two moment sets that prior work treated separately: the cross-sectional wealth shares (top-1% share = 33.6% in the 2007 SCF) and the intergenerational social mobility matrix (Shorrocks index 0.88 in Charles–Hurst’s PSID-based transition matrix). The estimated model fits both: top-1% share = 32.5%, Shorrocks = 0.92. Joint targeting is what disentangles the three channels: stochastic earnings drive mobility, while heterogeneous returns and differential savings (via bequest curvature ) drive levels. Without the mobility moments, the three channels are not separately identified.

Why Econ-ARK cares. The paper’s heterogeneous-return Markov chain is a natural fit for HARK’s existing Markov-chain exogenous-state machinery, and the dynasty-level structure extends buffer-stock theory into the intergenerational domain that underlies most modern inequality-measurement work.

What a REMARK of this paper would enable. Counterfactual wealth-tax and policy experiments, and extensions incorporating the demographic, mortality, and medical-risk features that the paper’s own “Limitations” section identifies as out of scope.

Prior Literature¶

Overview¶

Benhabib et al. (2019) builds on a rich tradition of heterogeneous-agent macroeconomic models that seek to explain the observed distribution of wealth in the United States. The foundational framework originates with Bewley (1983), who introduced incomplete-markets models in which agents self-insure against idiosyncratic income shocks. Huggett (1993) and Aiyagari (1994) extended this framework into general equilibrium, establishing the workhorse “Bewley-Huggett-Aiyagari” class of models. While these models successfully generate wealth dispersion, they consistently underpredict the concentration of wealth at the very top of the distribution — the thick right tail observed empirically.

Several strands of subsequent research sought to close this gap. Quadrini (2000) and Cagetti & De Nardi (2006) introduced entrepreneurship and its associated return heterogeneity as a mechanism for generating extreme wealth. Castañeda et al. (2003) showed that calibrating to a highly skewed earnings process could improve the fit to the upper tail. De Nardi (2004) demonstrated that voluntary bequests — particularly luxury bequests that grow with wealth — are important for transmitting large estates across generations. In parallel, Benhabib et al. (2011) and Benhabib et al. (2015) developed analytical results showing that stochastic returns to capital, combined with finite lifetimes and bequests, can generate Pareto-tailed stationary wealth distributions. These theoretical predictions found their empirical counterpart in Fagereng et al. (2020), who used Norwegian tax-record microdata to document substantial heterogeneity and persistence in individual returns to wealth — precisely the stochastic- process that Benhabib et al. (2019) identifies as a key driver of the upper tail of U.S. wealth.

Key Foundational Papers¶

Aiyagari (1994) — Established the canonical incomplete-markets model with idiosyncratic earnings risk and a borrowing constraint, showing how precautionary saving generates wealth accumulation but fails to match the top of the distribution.

De Nardi (2004) — Introduced voluntary (luxury) bequest motives into a life-cycle model, demonstrating that intergenerational transfers are essential for matching the concentration of wealth among the richest households.

Benhabib et al. (2011) — Proved analytically that models with stochastic capital income and intergenerational wealth transfers generate Pareto-tailed stationary distributions, providing the theoretical foundation for the quantitative exercise in Benhabib et al. (2019).

Castañeda et al. (2003) — Showed that a carefully calibrated earnings process with very high realizations (“superstar” earnings) can help match the U.S. wealth distribution, highlighting the role of labor income heterogeneity.

Krusell & Smith (1998) — Introduced discount-factor heterogeneity as an alternative mechanism for generating wealth inequality in general-equilibrium models, demonstrating that even small differences in patience can produce large differences in wealth.

Fagereng et al. (2020) — Used Norwegian tax-record microdata to document heterogeneity and persistence in individual returns to wealth, providing the empirical anchor for the stochastic-return channel that Benhabib et al. (2019) uses to explain the upper tail of the wealth distribution.

The Gap This Paper Addresses¶

Prior models typically focused on one or two mechanisms for wealth concentration — earnings risk alone (Aiyagari (1994); Castañeda et al. (2003)), bequest motives alone (De Nardi (2004)), or return heterogeneity in isolation (Quadrini (2000); Cagetti & De Nardi (2006)). While each mechanism could partially account for the thick tail of the wealth distribution, no single channel was sufficient. Moreover, earlier work had not jointly estimated all three channels within a unified framework that also matched social mobility patterns — the transition probabilities governing how families move across wealth brackets over generations.

Benhabib et al. (2019) fills this gap by embedding all three mechanisms — skewed earnings, heterogeneous returns to wealth, and wealth-dependent saving rates (via bequest motives) — into a single quantitative life-cycle model. Using the method of simulated moments, they estimate the model to jointly match the cross-sectional wealth distribution and intergenerational mobility matrices from the Survey of Consumer Finances. This allows them to decompose the relative contribution of each factor, revealing that capital income risk and differential savings are the primary drivers of the upper tail, while stochastic earnings are essential for matching social mobility.

Summary¶

Headline result. A standard lifecycle model with three structural channels — skewed lifecycle earnings, wealth-dependent bequest motives, and heterogeneous stochastic returns — jointly matches both the U.S. wealth distribution and the intergenerational social mobility matrix:

Top-1% wealth share: 32.5% model vs 33.6% data (2007 SCF; paper Table 5).

Social mobility — Shorrocks index 0.92 model vs 0.88 data (Charles–Hurst 2003 / PSID; transition diagonal: 0.349, 0.197, 0.201, 0.210, 0.340 model vs 0.36, 0.24, 0.25, 0.26, 0.36 data).

(Fit at the bottom of the wealth distribution is weaker — the model overshoots the lower quintiles — but the paper’s primary contribution is the upper-tail and mobility match.)

What identifies the three channels. Joint targeting of both moment sets is the methodological key. Without the mobility moments, the three channels are not separately identified — different combinations of return heterogeneity, bequest curvature, and earnings risk produce similar wealth-share patterns. Adding the social mobility matrix breaks the symmetry: stochastic earnings drive mobility (the channel that moves households across wealth quintiles across generations), while heterogeneous returns and differential savings drive the level of wealth in the upper tail. Estimation is by method of simulated moments — 12 moments matching 12 estimated parameters, exactly identified (with , , fixed externally; estimated parameters are , , the five-state space, and the diagonal of the -transition matrix).

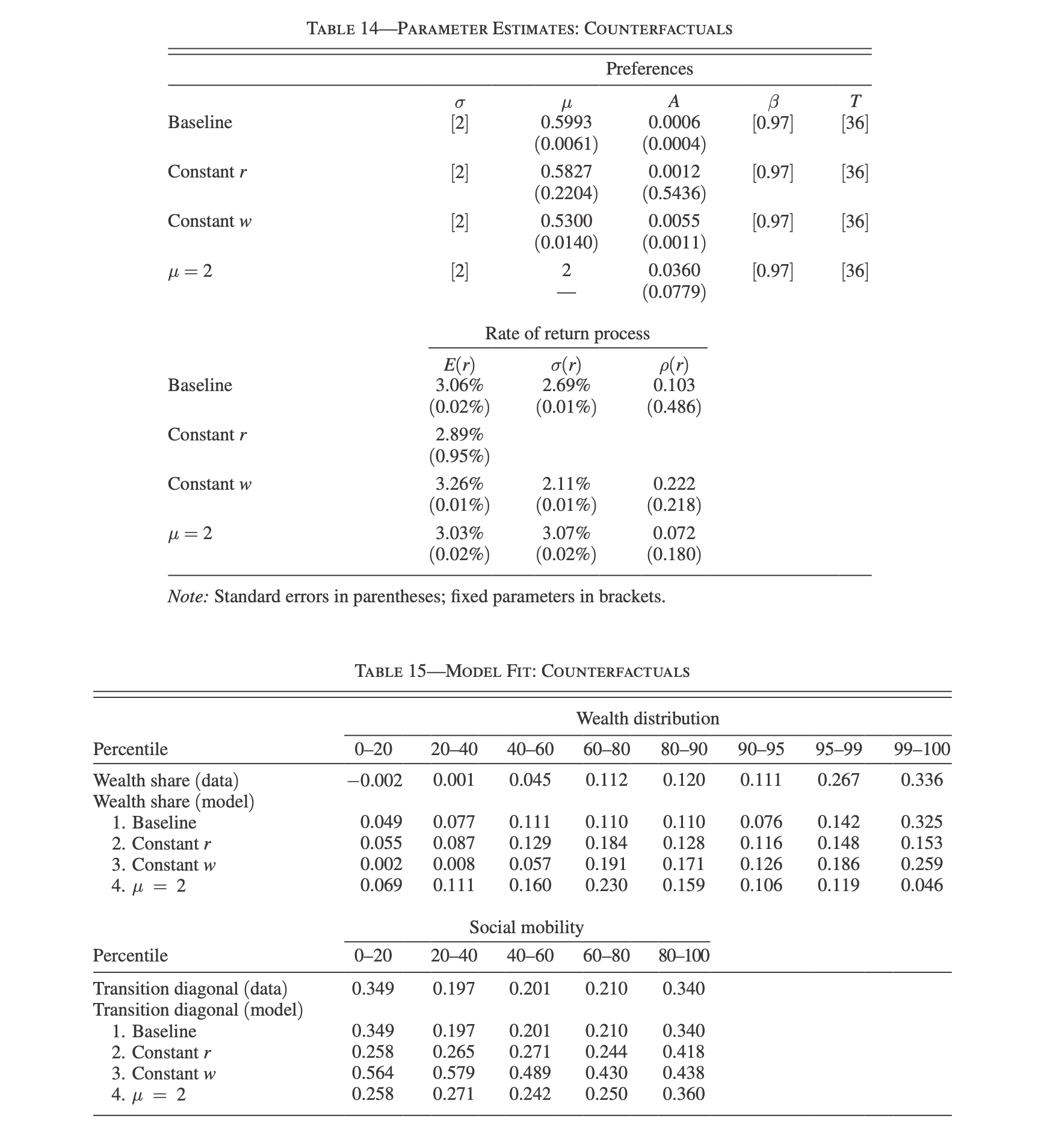

Quantitative decomposition (paper §IV, Table 15). Counterfactuals shutting off one channel at a time:

No return heterogeneity — bequest weight doubles to compensate; model fails the upper tail of the wealth distribution.

No stochastic earnings — wealth shares stay close to baseline, but the social mobility fit collapses; stochastic earnings are essential for mobility, not for the right tail.

Homogeneous savings (, no bequest curvature) — bequest weight rises further; capital-income channel must do all the work; upper-tail fit deteriorates substantially.

Bottom line. Capital income risk and differential savings (via bequest curvature ) drive the upper tail. Stochastic earnings drive social mobility. The joint-targeting identification is what enables this attribution.

For a detailed discussion of the foundational literature, see the Prior Literature notebook. For how later work addresses these issues, see the Subsequent Literature notebook.

Reading the formalization layer. This entry includes parallel technical artifacts that lift the model into a structured, machine-readable form (the Formalized tier per the ballpark spec). The YAML files are written in dolo-plus, a modular-DP YAML format used by the Bellman-DDSL ecosystem; they were produced by iteration with Matsya (a DDSL-aware evaluator) starting from the corresponding excerpt. Two parallel pairs:

Within-life:

bellman-excerpt.md(modular-DDSL Bellman statement: symbol table, perch decomposition, transitions, movers, EGM channel) +dolo-plus-draft.yaml(dolo-plus YAML, paper-calibrated from Tables 1, 4 + online Appendix C.1’s ).Dynasty:

dynasty-excerpt.md(cross-generational composition: lifetime map , joint chain , paper’s Pareto-tail Proposition) +dolo-plus-dynasty.yaml(YAML encoding).

Inline # unresolved: comments in the YAMLs mark places where the dolo-plus spec has no canonical idiom yet — structural intent is paper-faithful even where keyword names may need to be renamed once the spec stabilizes. verification.md compares the YAML to the paper section by section; bellman-excerpt.md Open Issues #1–#10 record the construction audit trail (notably Issue #10, where the published §I budget equation was found inconsistent with its own constraint and the online-Appendix-A.1 model was adopted instead).

Non-Technical Methodological Overview¶

The paper develops a macroeconomic model to explore wealth accumulation, distribution, and social mobility in the U.S., focusing on three main forces:

Stochastic Earnings: Research shows income variability plays a key role in wealth inequality, affecting saving decisions and consumption patterns, particularly for the bottom 60% of households. However, it does not account for the wealth concentration among the wealthiest. The incomplete-markets literature pioneered by Aiyagari (1994) established this channel.

Heterogeneous Rate of Return: Studies have identified significant variations in the risk-adjusted returns on investments across households, contributing to the wealth distribution’s long tail. This variation is consistent over time and linked with entrepreneurial activity Quadrini, 2000Cagetti & De Nardi, 2006.

Differential saving rates across wealth levels: The model includes increasing bequest motives with wealth, suggesting a stronger saving motive among the wealthiest, who aim to leave significant assets for their heirs. This perpetuates the transfer of large estates through generations, as emphasized by De Nardi (2004).

The analysis finds that stochastic earnings, differential savings, and capital income risk critically shape the wealth distribution’s tail and social mobility. Capital income risk and differential savings widen the wealth distribution’s tail and influence mobility, particularly enhancing it at the top end but reducing upward mobility from the bottom 20%. Despite being less impactful in the tail, stochastic earnings are vital for overall wealth mobility. Additionally, their findings suggest a wealth-dependent return rate enhances model fit across the wealth distribution.

The Model¶

A fairly simple microfounded model of lifecycle consumption and savings. Each agent’s life span is finite and deterministic, T years.

Features of the model¶

Every period, agents choose how much to consume (); end-of-period savings (and so next-period beginning wealth ) follow from the budget identity.

All agents are subjected to a no-borrowing constraint.

Agents leave bequests at the end of life T.

Wealth accumulates from savings and bequests.

Each agent is assigned at birth (i) a lifetime earnings-profile type drawn from a 10-state intergenerational Markov chain (paper Table 1 gives the ten decile-specific age profiles; Chetty et al. 2014 gives the intergenerational transition), and (ii) a rate-of-return state drawn from a 5-state Markov chain (see “Stochastic Structure” below). Both and are constant within a life, and each is stochastic across generations through its own intergenerational Markov chain, possibly correlated with that of the parent.

Preferences¶

Preferences are composed of:

per period utility from consumption

warm-glow utility from bequests at T,

Recursive Formulation¶

Given a type assignment drawn at birth and initial wealth , the agent’s optimization problem for is (following the paper’s online Appendix A.1 — the authors’ authoritative description of the numerical solution):

with terminal condition

Notation convention and source. This formulation follows online Appendix A.1. The published paper §I writes the budget compactly as with constraint , which is internally inconsistent: the constraint is genuine under the appendix model, but the budget equation as printed in §I is missing a factor on . The Formalized-tier artifacts in this directory (bellman-excerpt.md, dolo-plus-draft.yaml, dynasty-excerpt.md, dolo-plus-dynasty.yaml) build on the appendix model; see bellman-excerpt.md Open Issue #10 for the full audit trail.

For the dolo-plus three-perch decomposition used in bellman-excerpt.md, the arrival-perch state is (beginning-of-period wealth), the decision-perch state is identity with ( — just a perch label, no transformation), the control is , and the continuation-perch state is . Savings earn return , then earnings arrive at the end of the period.

Family structure. The household problem is a parameterized family of Bellman problems indexed by — ten earnings-profile types and five rate-of-return states, so fifty separate fixed-point problems in the baseline calibration. This is structurally analogous to HAFiscal’s type-indexed family (Carroll, Crawley, Frankovic, Tretvoll). Across generations, evolve according to the intergenerational Markov chains specified in “Stochastic Structure” below; within a life, they are fixed parameters of the value function, not state variables. A dolo-plus YAML must therefore either (a) encode the stage as a parameterized family with as calibration overrides across stage instances, or (b) encode the dynasty-level structure explicitly with as discrete states resolved only at birth — HAFiscal uses (a).

Stochastic Structure¶

Across generations, the paper specifies:

Rate of return is drawn from a finite -state Markov chain with transition . In the paper’s baseline , with off-diagonal probabilities restricted to decay geometrically away from the diagonal (except the last row, which uses constant off-diagonal probabilities); see paper §I and footnote 13. The full 5×5 matrix is in online Appendix C.1; transcribed in

dolo-plus-draft.yamlundercalibration_family.population.Pi_r.matrix.Earnings-profile type is drawn from a 10-state intergenerational Markov chain, calibrated from Chetty et al. (2014). The ten profile shapes are reported in paper Table 1 (transcribed into

dolo-plus-draft.yamlundercalibration_family.by_tau). Online Appendix B.2 describes the procedure for collapsing Chetty et al.'s 100×100 matrix to 10×10 but does not tabulate the result; the matrix would need separate reconstruction from Chetty et al.'s data tables or from the BBL replication package.and are independent of each other, but each is serially correlated across generations.

Extension (Section IIID): the paper also considers an extension in which the Markov state space of is allowed to depend on the agent’s initial wealth , capturing the empirically supported tendency for higher rates of return among the wealthy.

The solution to the above problem is a stochastic difference equation for the initial wealth of dynasties, induced by the processes, mapping into , where superscripts correspond to the nth generation:

Under the given assumptions of the model, the following holds:

If the stochastic process has a stationary distribution with a Pareto right tail

If savings rate increases with wealth, is convex in initial wealth (the rich save proportionally more); a stationary distribution might not exist, but if it does the right tail is at least as thick as Pareto.

The dynasty-level composition — including the lifetime map , the independence of the - and -chains, and the paper’s stationary-distribution Proposition — is formalized in dynasty-excerpt.md and dolo-plus-dynasty.yaml.

Quantitative Analysis¶

The paper uses the method of simulated moments (MSM) to identify unknown parameters.

Externally calibrate some parameters of the model

Estimate remaining parameters of the model by matching the targeted moments generated by the stationary distribution induced by the model and those in the data

Results¶

At the estimated parameter values, the model-induced wealth distribution closely resembles the wealth distribution in the data.

The estimates point to the existence of differential saving behavior (bequest motives)

Capital income risk is an important factor in driving wealth inequality

Next, the paper shuts down each of the three main factors listed above. The objective of this counterfactual exercise is to gauge the relative importance of the three mechanisms in driving the distribution of wealth.

Summary of Counterfactuals¶

No rate of return heterogeneity higher bequest motive (A doubles relative to baseline) & model can’t match the upper tail of the wealth distribution (Table-15-row(3))

No stochastic earnings relative preference for bequests while nothing else changes substantially & model does not miss as much in mimicking the upper tail of the wealth distribution stochastic earnings not driving the behavior of the right tail of wealth distribution.

However, social mobility matrix fit implied by this counterfactual is bad stochastic earnings matter for social mobility

Homogeneous saving rates preference for bequests , capital income is riskier & extremely bad fit in matching the upper tail of the wealth distribution

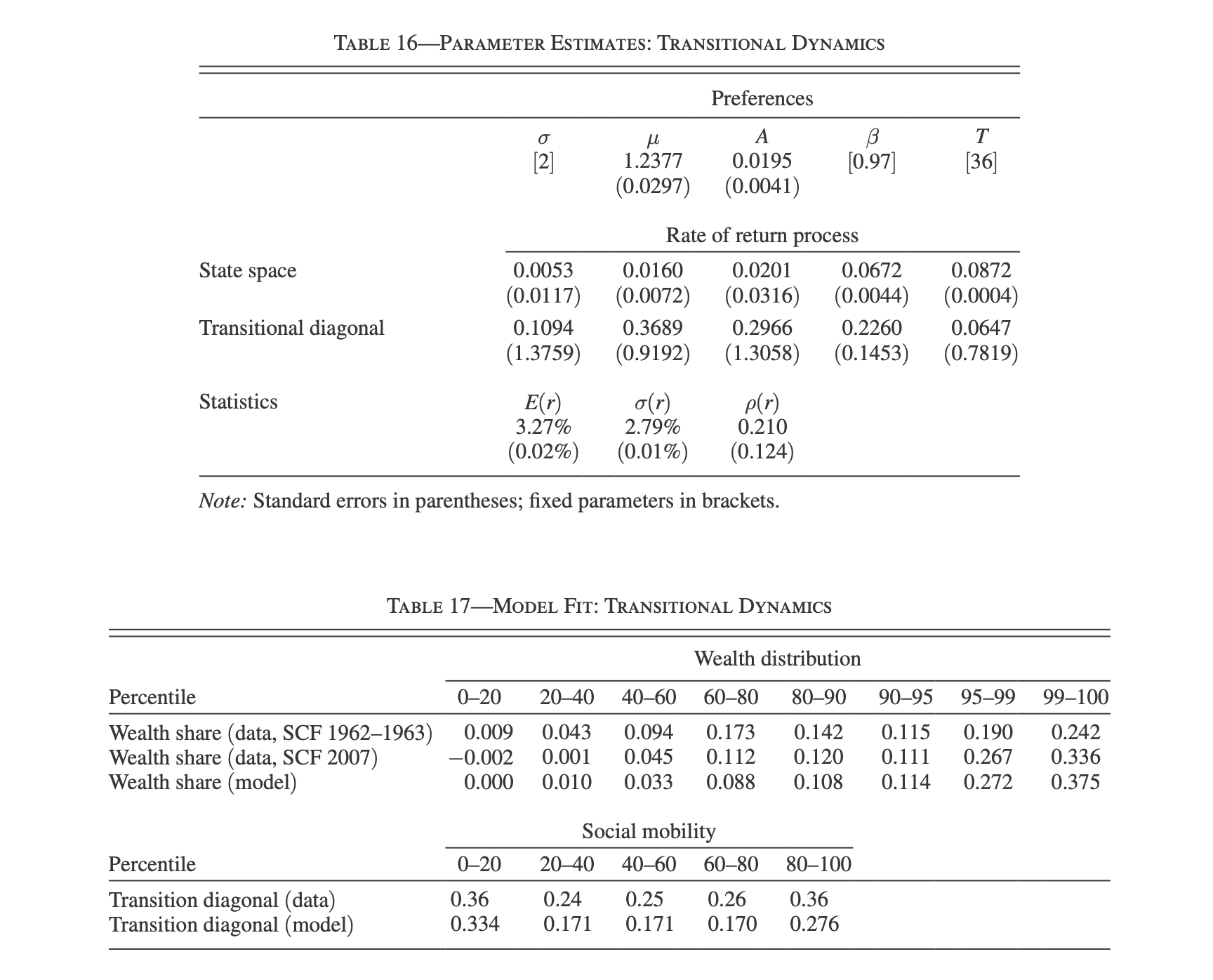

Lastly, the paper describes transitional dynamics of the wealth distribution within the confines of the model. In particular, the paper conducted an analysis using the SCF 1962–1963 wealth distribution as a starting point, estimating model parameters to match with the 2007 SCF distribution and previously used transition matrices. The findings highlight a significant rise in wealth inequality during this period, with the top 1% share increasing from 24.2% to 33.6%. The updated estimates reveal that this surge in inequality can be traced through enhanced capital income risk and differential savings, resulting in a skewed wealth distribution that closely matches empirical data, especially at the higher end. However, this model overestimates social mobility across wealth brackets.

Conclusion¶

The authors developed a standard macroeconomic model to explore the distribution of wealth in the United States, with a specific focus on the distribution’s tail. The model is notable for its ability to closely fit the observed data across the entire wealth spectrum and accurately capture the social mobility trends. Through their analysis, the authors successfully identified three key factors contributing to wealth accumulation: skewed and persistent earnings distribution, differential saving and bequest rates across wealth levels, and capital income risk associated with entrepreneurship. Each factor plays a distinct and empirically validated role in shaping both the wealth distribution and mobility. The paper also delves into the transitional dynamics of wealth distribution, with preliminary findings suggesting rapid changes over time, indicating promising areas for future research.

Limitations¶

The model ignores the following key features that are relevant for a proper quantitative study:

Overlapping generation demographic structure, which is crucial for modeling accidental bequests

Permanent income heterogeneity and within-lifetime permanent income risk (important for capturing savings done to counter that risk)

Luxury-type bequest motives. In their absence, even agents located at the lower end of the wealth distribution save for leaving bequests, but that is not supported by data. Luxury-type bequest motives can solve that problem.

Mortality risk, which again alters the saving behavior of retirees

Medical risk

Subsequent Literature¶

Research Directions Since Benhabib, Bisin, and Luo (2019)¶

Since the publication of Benhabib et al. (2019), the literature on wealth inequality has expanded in several directions. A major theme has been the further investigation of heterogeneous returns to capital as a driver of wealth concentration. Brüggemann & Mahone (2025) extend the analysis by estimating entrepreneurial rates of return and their implications for the wealth distribution, while Wolff (2024) examines whether the rich earn systematically higher returns on housing assets. Gomez (2025) connects wealth inequality to asset pricing, showing how the concentration of wealth affects equilibrium asset prices and returns.

A second strand of work has focused on the dynamics and tail behavior of the wealth distribution. Atkeson & Irie (2022) study the rapid changes in top wealth shares and the role of family firms in generating self-made fortunes, a phenomenon the static cross-sectional approach of Benhabib et al. (2019) was not designed to capture. Singh & Singh (2023) zoom in on the extreme right tail — the top 0.0003 percent — documenting its short-run dynamics. On the theoretical side, Lopez-Velasco (2025) develops an OLG model that endogenously generates distinct power laws in both earnings and wealth, and Birkner et al. (2022) study Pareto-distributed wealth dynamics in an open-economy setting.

A third direction concerns the macroeconomic and policy implications of wealth inequality. Andersen et al. (2024) study how pension reforms affect wealth concentration through intergenerational transfers. Cui & Miao (2025) analyze optimal taxation of sudden capital income surges — precisely the kind of capital income risk that Benhabib et al. (2019) identified as a key driver of the upper tail. Macnamara et al. (2023) use structural estimation to assess how marginal tax rates affect the long-run income and wealth distribution.

Key Subsequent Papers¶

Atkeson & Irie (2022) — Show that the rapid rise of self-made fortunes and family firms can explain much of the dynamics in top wealth shares, complementing the steady-state analysis in Benhabib et al. (2019).

Gomez (2025) — Establishes a link between wealth inequality and asset prices, demonstrating that the distribution of wealth has first-order effects on equilibrium returns.

Brüggemann & Mahone (2025) — Estimate heterogeneous entrepreneurial returns to wealth using U.S. microdata, finding that return heterogeneity is even more important for the upper tail than earlier calibrations suggested.

Benhabib et al. (2021) — Extend the Benhabib et al. (2019) framework to study long-run social mobility across heterogeneous dynasties, showing how persistence in returns and bequests shapes intergenerational wealth transmission.

Kaymak et al. (2026) — Develop a quantitative model that accounts for the rise in U.S. wealth concentration since the 1980s, incorporating multiple channels (tax changes, earnings inequality, and return heterogeneity) in a unified framework.

Open Questions and Gaps¶

Despite substantial progress, several questions remain open:

Within-lifetime return dynamics. Benhabib et al. (2019) assumed that an agent’s rate of return is fixed within their lifetime but stochastic across generations. Emerging evidence from Snudden (2025) on idiosyncratic asset returns suggests that within-lifetime variation in returns may be quantitatively important and could alter both the stationary distribution and mobility patterns.

Behavioral heterogeneity. Li et al. (2024) introduce present-biased preferences and show they affect the marginal propensity to consume and the wealth distribution. Whether behavioral heterogeneity is a substitute for, or complement to, the structural channels in Benhabib et al. (2019) remains an open question.

Differential fertility. Cooke et al. (2024) show that fertility differences across wealth groups interact with intergenerational transfers to shape long-run inequality — a channel absent from the Benhabib-Bisin-Luo framework.

Global and open-economy dimensions. Most of the literature, including Benhabib et al. (2019), studies a closed economy. Birkner et al. (2022) take a step toward open-economy analysis, but the interaction between capital mobility, return heterogeneity, and domestic wealth concentration remains largely unexplored.

Demand-side effects. Cavallari et al. (2025) study how wealth inequality feeds back into aggregate demand and the business cycle — a macroeconomic channel that the partial-equilibrium structure of Benhabib et al. (2019) does not capture.

- Benhabib, J., Bisin, A., & Luo, M. (2019). Wealth Distribution and Social Mobility in the US: A Quantitative Approach. American Economic Review, 109(5), 1623–1647. 10.1257/aer.20151684

- Bewley, T. (1983). A Difficulty with the Optimum Quantity of Money. Econometrica, 51(5), 1485–1504.

- Huggett, M. (1993). The Risk-Free Rate in Heterogeneous-Agent Incomplete-Insurance Economies. Journal of Economic Dynamics and Control, 17(5–6), 953–969.

- Aiyagari, S. R. (1994). Uninsured Idiosyncratic Risk and Aggregate Saving. Quarterly Journal of Economics, 109(3), 659–684.

- Quadrini, V. (2000). Entrepreneurship, Saving, and Social Mobility. Review of Economic Dynamics, 3(1), 1–40.

- Cagetti, M., & De Nardi, M. (2006). Entrepreneurship, Frictions, and Wealth. Journal of Political Economy, 114(5), 835–870.

- Castañeda, A., Díaz-Giménez, J., & Ríos-Rull, J.-V. (2003). Accounting for the U.S. Earnings and Wealth Inequality. Journal of Political Economy, 111(4), 818–857.

- De Nardi, M. (2004). Wealth Inequality and Intergenerational Links. Review of Economic Studies, 71(3), 743–768.

- Benhabib, J., Bisin, A., & Zhu, S. (2011). The Distribution of Wealth and Fiscal Policy in Economies with Finitely Lived Agents. Econometrica, 79(1), 123–157.

- Benhabib, J., Bisin, A., & Zhu, S. (2015). The Wealth Distribution in Bewley Economies with Capital Income Risk. Journal of Economic Theory, 159, 489–515.

- Fagereng, A., Guiso, L., Malacrino, D., & Pistaferri, L. (2020). Heterogeneity and Persistence in Returns to Wealth. Econometrica, 88(1), 115–170.

- Krusell, P., & Smith, A. A. (1998). Income and Wealth Heterogeneity in the Macroeconomy. Journal of Political Economy, 106(5), 867–896.

- Brüggemann, B., & Mahone, Z. L. (2025). Entrepreneurial Rates of Return and Wealth Inequality. Review of Economic Dynamics. 10.1016/j.red.2025.101298

- Wolff, E. N. (2024). Heterogeneous Rates of Return on Homes: Do the Rich Do Better? Review of Income and Wealth. 10.1111/roiw.12704

- Gomez, M. (2025). Wealth Inequality and Asset Prices. Review of Economic Studies. 10.1093/restud/rdaf008