A notebook by Christopher D. Carroll and Mateo Velásquez-Giraldo¶

Inspired by its Quantecon counterpart¶

This notebook presents simple computational tools to solve an instance of Lucas’s asset-pricing model for which there is no analytical solution: The case when the logarithm of the asset’s dividend follows an autoregressive process of order 1,

A presentation of this model can be found in Christopher D. Carroll’s lecture notes.

Those notes use the Bellman equation to derive a relationship between the price of the asset in the current period and the next period :

The equilibrium pricing equation is a relationship between the price and the dividend (a “pricing kernel”) such that, if everyone believes that to be the pricing kernel, everyone’s Euler equation will be satisfied:

As noted in the handout, there are some special circumstances in which it is possible to solve for analytically:

| Shock Process | Mean Restrictions | CRRA | Solution for Pricing Kernel |

|---|---|---|---|

| bounded, IID, | 1 (log) | ||

| lognormal, mean 1 | |||

| lognormal mean |

However, under most circumstances, the only way to obtain the pricing function is by solving for it numerically, as outlined below.

Finding the equilibrium pricing function.¶

We know that the equilibrium pricing function must satisfy the equation above. Let’s define an operator that allows us to evaluate whether any candidate pricing function satisfies this requirement.

Let be an operator which takes as argument a function and returns another function (these are usually called functionals or higher-order functions). For some function , denote with the function that results from applying to . Then, for any real number , will be the real number that one obtains when the function is given as an input.

We define our particular operator as follows. For any function , is obtained as

We can use to re-express our pricing equation. If is our equilibrium pricing funtion, it must satisfy

or, expressed differently,

Our equilibrium pricing function is therefore a fixed point of the operator .

It turns out that is a contraction mapping. This is useful because it implies, through Banach’s fixed-point theorem, that:

has exactly one fixed point.

Starting from an arbitrary function , the sequence converges to that fixed point.

For our purposes, this translates to:

Our equilibrium pricing function not only exists, but is unique.

We can get arbitrarily close to the equilibrium pricing function by making some initial guess and applying the operator to it repeatedly.

The code below creates a representation of our model and implements a solution routine to find . The main components of this routine are:

priceOnePeriod: this is operator from above. It takes a function , computes for a grid of values, and uses the result to construct a piecewise linear interpolator that approximates .solve: this is our iterative solution procedure. It generates an initial guess and appliespriceOnePeriodto it iteratively. At each application, it constructs a measure of how much the candidate pricing function changed. Once changes between successive iterations are small enough, it declares that the solution has converged.

A computational representation of the problem and its solution.¶

Uninteresting setup:

# Setup

import numpy as np

import matplotlib.pyplot as plt

from copy import copy

from HARK.rewards import CRRAutilityP

from HARK.distributions import Normal, expected

from HARK.interpolation import LinearInterp, ConstantFunction# A python class representing log-AR1 dividend processes.

class DivProcess:

def __init__(self, α, σ, γ=0.0, nApprox=7):

self.α = α

self.σ = σ

self.γ = γ

self.nApprox = nApprox

# Create a discrete approximation to the random shock

self.ShkAppDstn = Normal(mu=-(σ**2) / 2, sigma=σ).discretize(N=nApprox)

def getLogdGrid(self, n=100):

"""

A method for creating a reasonable grid for log-dividends.

"""

μ = self.γ - (self.σ**2) / 2

uncond_sd = self.σ / np.sqrt(1 - self.α**2)

uncond_mean = μ / (1 - self.α)

logDGrid = np.linspace(-5 * uncond_sd, 5 * uncond_sd, n) + uncond_mean

return logDGrid

# A class representing economies with Lucas trees.

class LucasEconomy:

"""

A representation of an economy in which there are Lucas trees

whose dividends' logarithm follows an AR1 process.

"""

def __init__(self, CRRA, DiscFac, DivProcess):

self.CRRA = CRRA

self.DiscFac = DiscFac

self.DivProcess = DivProcess

self.uP = lambda c: CRRAutilityP(c, self.CRRA)

def priceOnePeriod(self, Pfunc_next, logDGrid):

# Create a function that, given current dividends

# and the value of next period's shock, returns

# the discounted value derived from the asset next period.

def discounted_value(shock, log_d_now):

# Find dividends

d_now = np.exp(log_d_now)

log_d_next = self.DivProcess.γ + self.DivProcess.α * log_d_now + shock

d_next = np.exp(log_d_next)

# Payoff and sdf

payoff_next = Pfunc_next(log_d_next) + d_next

SDF = self.DiscFac * self.uP(d_next / d_now)

return SDF * payoff_next

# The price at a given d_t is the expectation of the discounted value.

# Compute it at every d in our grid. The expectation is taken over next

# period's shocks

prices_now = expected(

dstn=self.DivProcess.ShkAppDstn, func=discounted_value, args=(logDGrid,)

)

# Create new interpolating price function

Pfunc_now = LinearInterp(logDGrid, prices_now, lower_extrap=True)

return Pfunc_now

def solve(self, Pfunc_0=None, logDGrid=None, tol=1e-5, maxIter=500, disp=False):

# Initialize the norm

norm = tol + 1

# Initialize Pfunc if initial guess is not provided

if Pfunc_0 is None:

Pfunc_0 = ConstantFunction(0.0)

# Create a grid for log-dividends if one is not provided

if logDGrid is None:

logDGrid = self.DivProcess.getLogdGrid()

# Initialize function and compute prices on the grid

Pf_0 = copy(Pfunc_0)

P_0 = Pf_0(logDGrid)

it = 0

while norm > tol and it < maxIter:

# Apply the pricing equation

Pf_next = self.priceOnePeriod(Pf_0, logDGrid)

# Find new prices on the grid

P_next = Pf_next(logDGrid)

# Measure the change between price vectors

norm = np.linalg.norm(P_0 - P_next)

# Update price function and vector

Pf_0 = Pf_next

P_0 = P_next

it = it + 1

# Print iteration information

if disp:

print("Iter:" + str(it) + " Norm = " + str(norm))

if disp:

if norm <= tol:

print("Price function converged!")

else:

print("Maximum iterations exceeded!")

self.EqlogPfun = Pf_0

self.EqPfun = lambda d: self.EqlogPfun(np.log(d))Creating and solving an example economy with AR1 dividends¶

An economy is fully specified by:

The dividend process for the assets (trees): we assume that , . We must create a dividend process specifying and .

The coefficient of relative risk aversion (CRRA).

The time-discount factor ().

# Create a log-AR1 process for dividends

DivProc = DivProcess(α=0.90, σ=0.1)

# Create an example economy

economy = LucasEconomy(CRRA=2, DiscFac=0.95, DivProcess=DivProc)Once created, the economy can be ‘solved’, which means finding the equilibrium price kernel. The distribution of dividends at period depends on the value of dividends at , which also determines the resources agents have available to buy trees. Thus, is a state variable for the economy. The pricing function gives the price of trees that equates their demand and supply at every level of current dividends .

# Solve the economy, displaying the error term for each iteration

economy.solve(disp=True)

# After the economy is solved, we can use its Equilibrium price function

# to tell us the price if the dividend is 1

dvdnd = 1

print("P({}) = {:.6}".format(dvdnd, economy.EqPfun(dvdnd)))Iter:1 Norm = 14.34310594086344

Iter:2 Norm = 14.614867281705973

Iter:3 Norm = 14.81462233119635

Iter:4 Norm = 14.939364249843898

Iter:5 Norm = 14.989619417063073

Iter:6 Norm = 14.968432855040843

Iter:7 Norm = 14.880572667620452

Iter:8 Norm = 14.731927474014178

Iter:9 Norm = 14.52902047558161

Iter:10 Norm = 14.278638854628227

Iter:11 Norm = 13.987555448796973

Iter:12 Norm = 13.662325970904508

Iter:13 Norm = 13.309147997993502

Iter:14 Norm = 12.933769279362002

Iter:15 Norm = 12.54143477811982

Iter:16 Norm = 12.136863389363548

Iter:17 Norm = 11.724246791512238

Iter:18 Norm = 11.307264248656217

Iter:19 Norm = 10.88910839449017

Iter:20 Norm = 10.472518082357068

Iter:21 Norm = 10.059815280329328

Iter:22 Norm = 9.652943734511805

Iter:23 Norm = 9.253507730992833

Iter:24 Norm = 8.862809773368175

Iter:25 Norm = 8.481886375493007

Iter:26 Norm = 8.111541464653394

Iter:27 Norm = 7.752377114027517

Iter:28 Norm = 7.40482148881162

Iter:29 Norm = 7.069154009563337

Iter:30 Norm = 6.745527819188153

Iter:31 Norm = 6.43398969488094

Iter:32 Norm = 6.134497580005358

Iter:33 Norm = 5.846935928796937

Iter:34 Norm = 5.571129063207857

Iter:35 Norm = 5.306852739535748

Iter:36 Norm = 5.053844115275684

Iter:37 Norm = 4.8118102958592255

Iter:38 Norm = 4.5804356280614105

Iter:39 Norm = 4.359387892926313

Iter:40 Norm = 4.148323536855

Iter:41 Norm = 3.946892065541599

Iter:42 Norm = 3.7547397120884534

Iter:43 Norm = 3.5715124781038123

Iter:44 Norm = 3.3968586350059407

Iter:45 Norm = 3.23043076218392

Iter:46 Norm = 3.071887389099951

Iter:47 Norm = 2.92089429983745

Iter:48 Norm = 2.777125550947055

Iter:49 Norm = 2.6402642466621504

Iter:50 Norm = 2.5100031095739235

Iter:51 Norm = 2.386044879600522

Iter:52 Norm = 2.2681025694850425

Iter:53 Norm = 2.155899601045683

Iter:54 Norm = 2.049169842908783

Iter:55 Norm = 1.9476575674272367

Iter:56 Norm = 1.8511173418645133

Iter:57 Norm = 1.7593138666580201

Iter:58 Norm = 1.672021771624408

Iter:59 Norm = 1.5890253792862712

Iter:60 Norm = 1.510118443058598

Iter:61 Norm = 1.4351038667929092

Iter:62 Norm = 1.3637934111186265

Iter:63 Norm = 1.2960073911146144

Iter:64 Norm = 1.2315743690705385

Iter:65 Norm = 1.1703308454400114

Iter:66 Norm = 1.1121209505264746

Iter:67 Norm = 1.0567961389685152

Iter:68 Norm = 1.004214888688016

Iter:69 Norm = 0.9542424056244561

Iter:70 Norm = 0.9067503352925078

Iter:71 Norm = 0.8616164819572083

Iter:72 Norm = 0.818724536020655

Iter:73 Norm = 0.777963810043275

Iter:74 Norm = 0.7392289836834438

Iter:75 Norm = 0.7024198577214298

Iter:76 Norm = 0.6674411172382658

Iter:77 Norm = 0.634202103941166

Iter:78 Norm = 0.6026165975626904

Iter:79 Norm = 0.5726026062095858

Iter:80 Norm = 0.5440821654963686

Iter:81 Norm = 0.5169811462657242

Iter:82 Norm = 0.49122907067358845

Iter:83 Norm = 0.4667589363979194

Iter:84 Norm = 0.44350704871700236

Iter:85 Norm = 0.421412860193699

Iter:86 Norm = 0.4004188176968008

Iter:87 Norm = 0.3804702164882355

Iter:88 Norm = 0.3615150611045491

Iter:89 Norm = 0.3435039327628806

Iter:90 Norm = 0.32638986302583317

Iter:91 Norm = 0.31012821346309866

Iter:92 Norm = 0.2946765610546749

Iter:93 Norm = 0.27999458908628433

Iter:94 Norm = 0.2660439832949772

Iter:95 Norm = 0.2527883330301617

Iter:96 Norm = 0.24019303720337631

Iter:97 Norm = 0.2282252148079118

Iter:98 Norm = 0.21685361979727616

Iter:99 Norm = 0.20604856012013625

Iter:100 Norm = 0.19578182071641212

Iter:101 Norm = 0.18602659028839066

Iter:102 Norm = 0.1767573916672117

Iter:103 Norm = 0.16795001560349337

Iter:104 Norm = 0.15958145781814148

Iter:105 Norm = 0.1516298591567478

Iter:106 Norm = 0.14407444869702674

Iter:107 Norm = 0.13689548966714943

Iter:108 Norm = 0.1300742280379809

Iter:109 Norm = 0.1235928436590115

Iter:110 Norm = 0.1174344038138782

Iter:111 Norm = 0.11158281907722094

Iter:112 Norm = 0.10602280136006649

Iter:113 Norm = 0.10073982403589372

Iter:114 Norm = 0.09572008404579596

Iter:115 Norm = 0.09095046588484632

Iter:116 Norm = 0.08641850737699282

Iter:117 Norm = 0.08211236714998044

Iter:118 Norm = 0.07802079372731051

Iter:119 Norm = 0.07413309615584784

Iter:120 Norm = 0.07043911609430371

Iter:121 Norm = 0.06692920128960075

Iter:122 Norm = 0.06359418037268635

Iter:123 Norm = 0.06042533890809264

Iter:124 Norm = 0.057414396635407663

Iter:125 Norm = 0.054553485843217786

Iter:126 Norm = 0.05183513081936258

Iter:127 Norm = 0.049252228324352595

Iter:128 Norm = 0.04679802903643489

Iter:129 Norm = 0.04446611992096433

Iter:130 Norm = 0.04225040747722925

Iter:131 Norm = 0.040145101819746856

Iter:132 Norm = 0.03814470155217281

Iter:133 Norm = 0.03624397939444744

Iter:134 Norm = 0.03443796852609161

Iter:135 Norm = 0.03272194960916258

Iter:136 Norm = 0.031091438458342148

Iter:137 Norm = 0.029542174324315832

Iter:138 Norm = 0.028070108761445414

Iter:139 Norm = 0.02667139504984569

Iter:140 Norm = 0.025342378144178373

Iter:141 Norm = 0.024079585123435457

Iter:142 Norm = 0.022879716116425367

Iter:143 Norm = 0.021739635679333864

Iter:144 Norm = 0.020656364602714354

Iter:145 Norm = 0.019627072127070527

Iter:146 Norm = 0.018649068545766374

Iter:147 Norm = 0.01771979817680735

Iter:148 Norm = 0.016836832684830137

Iter:149 Norm = 0.015997864735649348

Iter:150 Norm = 0.015200701966844189

Iter:151 Norm = 0.014443261259211396

Iter:152 Norm = 0.013723563293191268

Iter:153 Norm = 0.013039727376824886

Iter:154 Norm = 0.012389966531120225

Iter:155 Norm = 0.011772582820757146

Iter:156 Norm = 0.011185962916935679

Iter:157 Norm = 0.01062857388152953

Iter:158 Norm = 0.010098959161571077

Iter:159 Norm = 0.009595734782801998

Iter:160 Norm = 0.00911758573331583

Iter:161 Norm = 0.008663262527145959

Iter:162 Norm = 0.008231577939258631

Iter:163 Norm = 0.007821403903143986

Iter:164 Norm = 0.007431668562953552

Iter:165 Norm = 0.007061353472598732

Iter:166 Norm = 0.006709490934464021

Iter:167 Norm = 0.0063751614704972495

Iter:168 Norm = 0.006057491419614152

Iter:169 Norm = 0.005755650654652022

Iter:170 Norm = 0.005468850413064407

Iter:171 Norm = 0.005196341235730253

Iter:172 Norm = 0.004937411008699256

Iter:173 Norm = 0.004691383101932497

Iter:174 Norm = 0.004457614601632301

Iter:175 Norm = 0.004235494629770892

Iter:176 Norm = 0.004024442748025629

Iter:177 Norm = 0.003823907440919708

Iter:178 Norm = 0.0036333646745771654

Iter:179 Norm = 0.003452316527362579

Iter:180 Norm = 0.0032802898888329274

Iter:181 Norm = 0.0031168352231918865

Iter:182 Norm = 0.002961525394785437

Iter:183 Norm = 0.0028139545518366246

Iter:184 Norm = 0.00267373706579672

Iter:185 Norm = 0.0025405065238508634

Iter:186 Norm = 0.0024139147712710584

Iter:187 Norm = 0.0022936310014923895

Iter:188 Norm = 0.0021793408920568543

Iter:189 Norm = 0.0020707457828244703

Iter:190 Norm = 0.0019675618956923836

Iter:191 Norm = 0.0018695195930966792

Iter:192 Norm = 0.0017763626732945814

Iter:193 Norm = 0.0016878477009181062

Iter:194 Norm = 0.001603743370814542

Iter:195 Norm = 0.001523829903624448

Iter:196 Norm = 0.0014478984714075974

Iter:197 Norm = 0.001375750651995658

Iter:198 Norm = 0.0013071979105175545

Iter:199 Norm = 0.001242061106635624

Iter:200 Norm = 0.0011801700264542725

Iter:201 Norm = 0.0011213629376277934

Iter:202 Norm = 0.0010654861670085145

Iter:203 Norm = 0.0010123936987695278

Iter:204 Norm = 0.0009619467929445259

Iter:205 Norm = 0.0009140136229716336

Iter:206 Norm = 0.0008684689310220655

Iter:207 Norm = 0.0008251937008250442

Iter:208 Norm = 0.0007840748465884144

Iter:209 Norm = 0.0007450049175648438

Iter:210 Norm = 0.0007078818171773037

Iter:211 Norm = 0.0006726085362432564

Iter:212 Norm = 0.0006390928994664652

Iter:213 Norm = 0.0006072473245952711

Iter:214 Norm = 0.0005769885936040177

Iter:215 Norm = 0.0005482376350572404

Iter:216 Norm = 0.0005209193177180375

Iter:217 Norm = 0.0004949622539685552

Iter:218 Norm = 0.00047029861347630916

Iter:219 Norm = 0.0004468639458267492

Iter:220 Norm = 0.0004245970121032102

Iter:221 Norm = 0.00040343962488112255

Iter:222 Norm = 0.00038333649621035825

Iter:223 Norm = 0.00036423509313689677

Iter:224 Norm = 0.00034608550026885444

Iter:225 Norm = 0.00032884028958809217

Iter:226 Norm = 0.0003124543962759582

Iter:227 Norm = 0.0002968850011565627

Iter:228 Norm = 0.00028209141866892884

Iter:229 Norm = 0.0002680349905576475

Iter:230 Norm = 0.0002546789849357291

Iter:231 Norm = 0.00024198850023253644

Iter:232 Norm = 0.0002299303738882025

Iter:233 Norm = 0.00021847309604241106

Iter:234 Norm = 0.00020758672670371484

Iter:235 Norm = 0.000197242817963524

Iter:236 Norm = 0.00018741433928826714

Iter:237 Norm = 0.00017807560717920262

Iter:238 Norm = 0.00016920221791301237

Iter:239 Norm = 0.00016077098373458665

Iter:240 Norm = 0.00015275987235465702

Iter:241 Norm = 0.00014514794933610434

Iter:242 Norm = 0.000137915323380576

Iter:243 Norm = 0.00013104309440237102

Iter:244 Norm = 0.00012451330400711154

Iter:245 Norm = 0.00011830888873856297

Iter:246 Norm = 0.00011241363536902475

Iter:247 Norm = 0.0001068121385326778

Iter:248 Norm = 0.00010148976060521523

Iter:249 Norm = 9.643259320029383e-05

Iter:250 Norm = 9.162742108566186e-05

Iter:251 Norm = 8.706168754619847e-05

Iter:252 Norm = 8.272346145365097e-05

Iter:253 Norm = 7.860140630130716e-05

Iter:254 Norm = 7.468475039819174e-05

Iter:255 Norm = 7.096325889746349e-05

Iter:256 Norm = 6.742720682601107e-05

Iter:257 Norm = 6.406735387874806e-05

Iter:258 Norm = 6.087492015769238e-05

Iter:259 Norm = 5.784156329083827e-05

Iter:260 Norm = 5.495935660985967e-05

Iter:261 Norm = 5.222076833999482e-05

Iter:262 Norm = 4.9618642107046365e-05

Iter:263 Norm = 4.7146178127042934e-05

Iter:264 Norm = 4.4796915380576354e-05

Iter:265 Norm = 4.256471482312034e-05

Iter:266 Norm = 4.044374335343422e-05

Iter:267 Norm = 3.8428458452395206e-05

Iter:268 Norm = 3.65135939085278e-05

Iter:269 Norm = 3.469414577592586e-05

Iter:270 Norm = 3.296535953101107e-05

Iter:271 Norm = 3.132271751942793e-05

Iter:272 Norm = 2.9761927333477716e-05

Iter:273 Norm = 2.827891023551752e-05

Iter:274 Norm = 2.686979091958857e-05

Iter:275 Norm = 2.5530887075460387e-05

Iter:276 Norm = 2.4258699903291916e-05

Iter:277 Norm = 2.304990500900857e-05

Iter:278 Norm = 2.1901343559741297e-05

Iter:279 Norm = 2.0810014136204545e-05

Iter:280 Norm = 1.9773064945727455e-05

Iter:281 Norm = 1.8787786251643173e-05

Iter:282 Norm = 1.7851603329965908e-05

Iter:283 Norm = 1.696206980654742e-05

Iter:284 Norm = 1.611686111768278e-05

Iter:285 Norm = 1.5313768645419402e-05

Iter:286 Norm = 1.4550693695290708e-05

Iter:287 Norm = 1.3825642320721789e-05

Iter:288 Norm = 1.313671972337381e-05

Iter:289 Norm = 1.2482125690853726e-05

Iter:290 Norm = 1.1860149638043228e-05

Iter:291 Norm = 1.126916627003413e-05

Iter:292 Norm = 1.0707631213278965e-05

Iter:293 Norm = 1.0174077062486109e-05

Iter:294 Norm = 9.667109531709195e-06

Price function converged!

P(1) = 20.1571

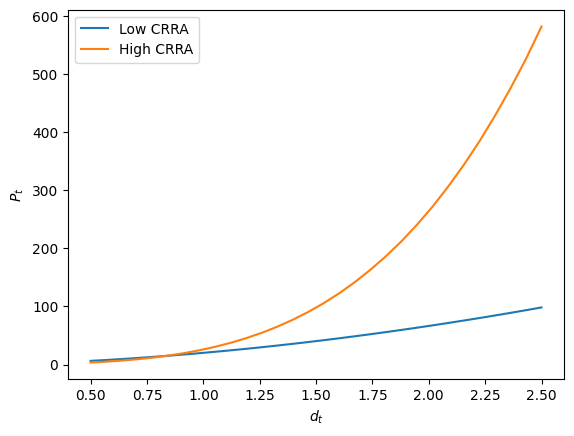

The effect of risk aversion.¶

The notes discuss the surprising implication that an increase in the coefficient of relative risk aversion leads to higher prices for the risky trees! This is demonstrated below.

# Create two economies with different risk aversion

Disc = 0.95

LowCRRAEcon = LucasEconomy(CRRA=2, DiscFac=Disc, DivProcess=DivProc)

HighCRRAEcon = LucasEconomy(CRRA=4, DiscFac=Disc, DivProcess=DivProc)

# Solve both

LowCRRAEcon.solve()

HighCRRAEcon.solve()

# Plot the pricing functions for both

dGrid = np.linspace(0.5, 2.5, 30)

plt.figure()

plt.plot(dGrid, LowCRRAEcon.EqPfun(dGrid), label="Low CRRA")

plt.plot(dGrid, HighCRRAEcon.EqPfun(dGrid), label="High CRRA")

plt.legend()

plt.xlabel("$d_t$")

plt.ylabel("$P_t$")

Testing our analytical solutions¶

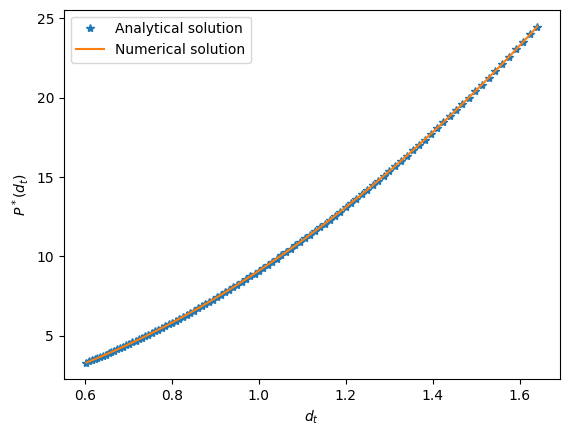

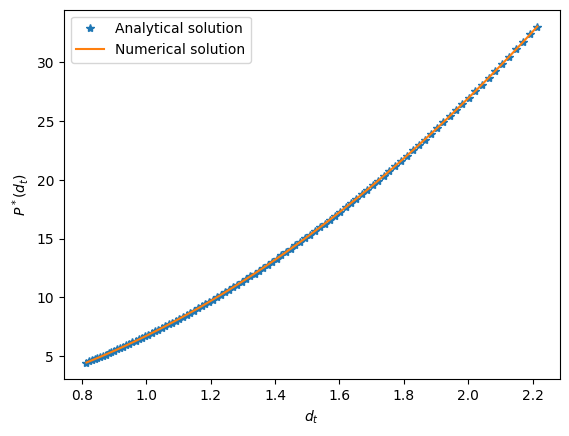

Case 1: Log Utility¶

The lecture notes show that with logarithmic utility (a CRRA of 1), the pricing kernel has a closed form expression:

.

We now compare our numerical solution with this analytical expression.

# Create an economy with log utility and the same dividend process from before

logUtilEcon = LucasEconomy(CRRA=1, DiscFac=Disc, DivProcess=DivProc)

# Solve it

logUtilEcon.solve()

# Generate a function with our analytical solution

theta = 1 / Disc - 1

def aSol(d):

return d / theta

# Get a grid for d over which to compare them

dGrid = np.exp(DivProc.getLogdGrid())

# Plot both

plt.figure()

plt.plot(dGrid, aSol(dGrid), "*", label="Analytical solution")

plt.plot(dGrid, logUtilEcon.EqPfun(dGrid), label="Numerical solution")

plt.legend()

plt.xlabel("$d_t$")

plt.ylabel("$P^*(d_t)$")

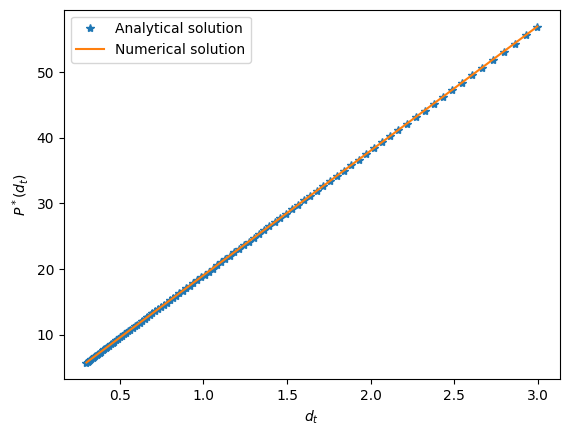

Case 2: I.I.D dividends¶

The notes also show that, if for all , the pricing kernel is exactly

We now our numerical solution for this case.

# Create an i.i.d. dividend process

σ = 0.1

iidDivs = DivProcess(α=0.0, σ=σ)

# And an economy that embeds it

CRRA = 2

Disc = 0.9

iidEcon = LucasEconomy(CRRA=CRRA, DiscFac=Disc, DivProcess=iidDivs)

iidEcon.solve()

# Generate a function with our analytical solution

dTil = np.exp((σ**2) / 2 * CRRA * (CRRA - 1))

def aSolIID(d):

return d**CRRA * dTil * Disc / (1 - Disc)

# Get a grid for d over which to compare them

dGrid = np.exp(iidDivs.getLogdGrid())

# Plot both

plt.figure()

plt.plot(dGrid, aSolIID(dGrid), "*", label="Analytical solution")

plt.plot(dGrid, iidEcon.EqPfun(dGrid), label="Numerical solution")

plt.legend()

plt.xlabel("$d_t$")

plt.ylabel("$P^*(d_t)$")

plt.show()

Case 3: Dividends that are a geometric random walk with drift¶

The notes also show that if the dividend process is

so that , then we have

which, when , reduces (as it should) to

CRRA = 2

Disc = 0.9

σ = 0.1

γ = 0.3

# Create a random walk dividend process

# (it turns out that the whole model can be normalized by d_t, and

# in normalized, terms the dividend proces becomes iid again)

rw_divs = DivProcess(γ=γ, α=0, σ=σ)

# And an economy that embeds it

rw_econ = LucasEconomy(CRRA=CRRA, DiscFac=Disc, DivProcess=rw_divs)

rw_econ.solve()

# Generate a function with our analytical solution

a_sol_factor = np.exp((CRRA - 1) * (CRRA * σ**2 / 2 - γ))

def a_sol_rw(d):

return d**CRRA * a_sol_factor * Disc / (1 - Disc)

# Get a grid for d over which to compare them

dGrid = np.exp(rw_divs.getLogdGrid())

# Plot both

plt.figure()

plt.plot(dGrid, a_sol_rw(dGrid), "*", label="Analytical solution")

plt.plot(dGrid, rw_econ.EqPfun(dGrid), label="Numerical solution")

plt.legend()

plt.xlabel("$d_t$")

plt.ylabel("$P^*(d_t)$")

plt.show()

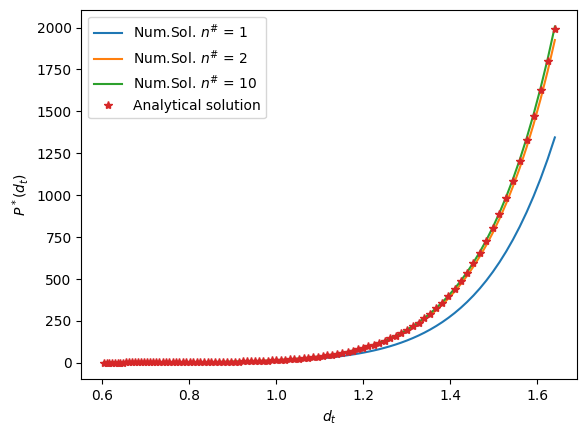

Testing our approximation of the dividend process¶

Hidden in the solution method implemented above is the fact that, in order to make expectations easy to compute, we discretize the random shock , which is to say, we create a discrete variable that approximates the behavior of . This is done using a Gauss-Hermite quadrature.

A parameter for the numerical solution is the number of different values that we allow our discrete approximation to take, . We would expect a higher n^# to improve our solution, as the discrete approximation of improves. We test this below.

# Increase CRRA to make the effect of uncertainty more evident.

CRRA = 10

Disc = 0.9

σ = 0.1

ns = [1, 2, 10]

dTil = np.exp((σ**2) / 2 * CRRA * (CRRA - 1.0))

def aSolIID(d):

return d**CRRA * dTil * Disc / (1 - Disc)

dGrid = np.exp(iidDivs.getLogdGrid())

plt.figure()

for n in ns:

iidDivs = DivProcess(α=0.0, σ=σ, nApprox=n)

iidEcon = LucasEconomy(CRRA=CRRA, DiscFac=Disc, DivProcess=iidDivs)

iidEcon.solve()

plt.plot(dGrid, iidEcon.EqPfun(dGrid), label="Num.Sol. $n^\#$ = {}".format(n))

# Plot both

plt.plot(dGrid, aSolIID(dGrid), "*", label="Analytical solution")

plt.legend()

plt.xlabel("$d_t$")

plt.ylabel("$P^*(d_t)$")

plt.show()